Inflation Is Set to Fall. The Fed Should Back Off.

Wage growth has been experiencing a historic slowdown. If that trend holds up, inflation is on track to get within half a percentage point of the Fed’s 2% target level by this time next year. But will inflation hawks be willing to take yes for an answer?

A man walks past price advertisements on windows of a grocery store in the Brooklyn borough of New York, the United States, on February 14, 2023. (Michael Nagle / Xinhua via Getty Images)

A little over a week ago, I tried to make the case for a more relaxed view of the current inflation situation than might be gleaned from the alarmist analyses emanating from top Fed officials and some prominent commentators — not least Jason Furman, former chief economist in the Obama administration and a notable voice of inflation hawkery. Responding to new data released late last month showing a sizable jump in the core inflation rate in January, Furman published an op-ed in the Wall Street Journal headlined “To Fight Inflation, Fed Tightening Should Go Faster and Further.”

My basic argument, as Eric Levitz of New York Magazine efficiently summed it up in a tweet, was that, “looking beyond a month-to-month time horizon, wage growth more or less determines price growth [and] wage growth is rapidly decelerating.”

I showed, first, that the correlation between wage growth and inflation, though not very impressive within a one-month or three-month timespan, becomes extremely strong at longer time horizons: the R-squared (i.e. the strength of the correlation) rises to 0.63 at a one-year horizon and 0.78 by four years.

Second, I showed that wages have indeed been rapidly decelerating — so rapidly, in fact, that in the forty-odd years since the massive disinflation engineered by former Fed chairman Paul Volcker in the early 1980s, only four months have seen faster wage deceleration (measured by the twelve-month change in the twelve-month growth rate) than what we experienced in January of this year. (And in three of those four other months, the data were clearly distorted by the pandemic shutdowns of spring 2020.)

Essentially, I’m saying that wages are a kind of “super-core” inflation index. Economists and policy makers pay close attention to measures of “core” inflation, which, in different ways, strip out the more volatile or transitory components of the product basket. There are core indexes that exclude just food and energy prices; others that try to more systematically identify and exclude the most volatile product categories; and still others that exclude the outliers (i.e. the products with the highest and lowest inflation rates each month, rather than those with the most volatile rates).

But in all cases, the idea is that by abstracting from the random noise and fleeting shocks that cause “headline” inflation to fluctuate so much, these indexes can give a better gauge of the underlying inflationary forces at work — and therefore a better clue to what inflation might do in the near future. In practice, what I’m arguing is that the rate of wage growth is the “most core” price index, as Elon Musk might put it.

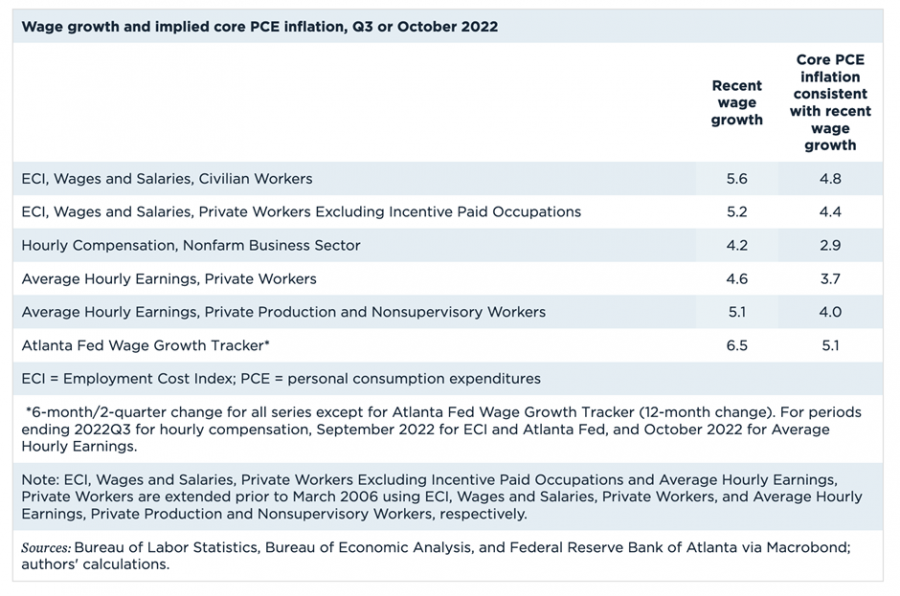

Furman, as a practical, policy-oriented economist, can hardly be said to lack awareness of the tight connection between wage growth and inflation. In fact, in an article he wrote for the Peterson Institute for International Economics last November, he carried out an interesting little statistical exercise that was premised on exactly this connection: he took five different measures of wage growth, and for each one, calculated the core Personal Consumption Expenditures (PCE) inflation rate “implied” (as he put it) by its current level. (Core PCE, the price index for household purchases excluding food and energy, is the measure to which the Fed tends to give the greatest weight when aiming to reach its 2 percent inflation target.)

According to Furman’s calculations, all five of the wage growth measures, as they stood in October 2022, were implying core inflation rates well above the Fed’s 2 percent target: they ranged from 2.9 percent to 5.1 percent, with a median of 4.2 percent. This finding, in his view, strengthens the case that the Fed needs to tighten even faster.

But surely if we want to judge whether monetary policy should be tightened further to stem inflation, we need to know not just the current rate of inflation but also its current trend. At the risk of stating the obvious: if the goal is disinflation, and if disinflation is already happening, then existing monetary conditions are already disinflationary. In that case, there’s no obvious reason to tighten further. The current level of inflation can’t tell you whether monetary policy is sufficiently disinflationary. For that you need to know the trend. This is where measures of core inflation can be useful: they can identify the underlying trend of inflation more clearly than it appears in the headline figure.

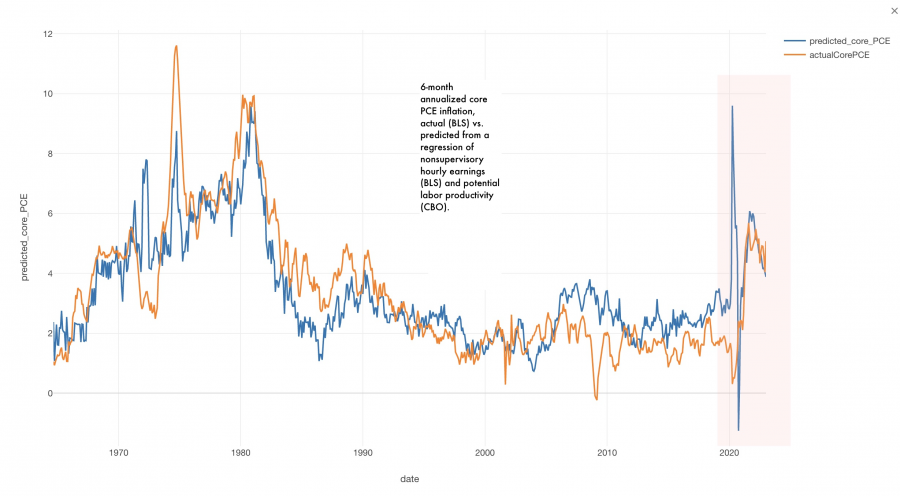

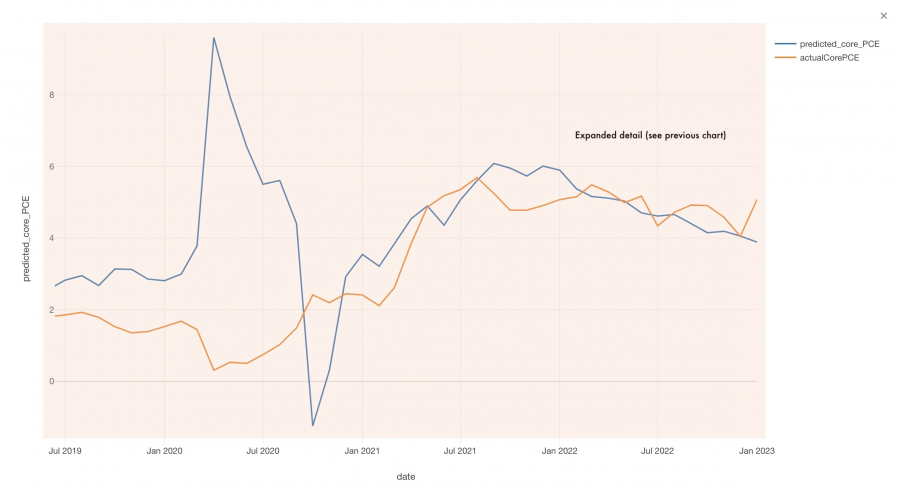

I thought it would be interesting to update Furman’s estimates of the inflation rates “implied” by the current rate of wage growth, but I couldn’t find an explanation of exactly how he had arrived at his results. So I just went ahead and used the simplest method that made sense to me: I ran a regression that used the rate of wage growth and the rate of trend labor productivity growth to predict the core PCE inflation rate. (Wages and labor productivity, taken jointly, are considered to be the main determinants of inflation in the theory of John Maynard Keynes, as I explained in an earlier article.) In the chart below, I compare this predicted core PCE inflation rate with the actual rate published by the Department of Commerce.

Three facts jump out from this exercise. First is the excellent fit of the data, which should be evident from the chart below: the lines showing actual versus predicted core inflation hug each other very closely. (The R-squared of the regression is a very respectable 0.64.) Once again, this shows that wages, jointly with productivity, have a preponderant influence on inflation.

Finally, and perhaps most importantly, over the past year the core PCE inflation rate implied by the rate of wage growth fell rapidly — from 5.4 percent in February 2022 to 4 percent in February 2023. At that pace of disinflation, we will reach a level of wage growth historically consistent with the Fed’s 2 percent inflation target rate in less than eighteen months — without the need for any additional tightening by the Fed.