The Latest Bout of Inflation Doom-Mongering Doesn’t Add Up

Last week’s inflation data prompted an outpouring of alarmism and calls for the Fed to squeeze the economy even harder. Here’s why the doomsaying is wrong.

Jerome Powell, chairman of the US Federal Reserve, speaks during a news conference in Washington, DC, on February 1, 2023. (Al Drago / Bloomberg via Getty Images)

Over the past few weeks I’ve been writing a series of articles about inflation and theories of inflation, and how and why those theories have changed over time. I’m not done yet — we’re only up to the late 1950s and Milton Friedman has only just made his appearance — but I think it’s worth pausing to take stock of the current inflation situation. What can those theories, and that history, tell us about the post-COVID outbreak of inflation we’re still dealing with today?

Last Friday, we got a new batch of inflation data, along with a few other key metrics, and the news was bad: the front-page headline in Saturday’s New York Times was, “Measure of Inflation Speeds Up, Muddling Hope of Easy Recovery.” The measure in question is the price index for household purchases — the Personal Consumption Expenditures, or PCE, price index — whose annualized growth rate jumped to 7.7% in January, compared to 2.4% the previous month. Core PCE, the Fed’s preferred inflation metric, which strips out food and energy prices, also jumped, rising to a 7.1% annualized rate, compared to 2.6% the previous month.

The Times write-up was gloomy: “There was a moment, late last year, when everything seemed to be going according to the Federal Reserve’s plan: Inflation was slowing, consumers were pulling back and the overheated economy was gently cooling down. But a spate of fresh data, including worrying figures released Friday, make it clear that the road ahead is likely to be bumpier and more treacherous than expected.”

Even more somber was Jason Furman, the former chair of the Council of Economic Advisers under Barack Obama, a frequent collaborator of Larry Summers’s who, like Summers, has been a prominent voice of inflation hawkery. (“The Fed Has to Stay the Course Against Inflation” was the headline of a Furman op-ed in the Wall Street Journal last October.)

“The economy is very overheated,” Furman tweeted shortly after last Friday’s data release:

The economy is very overheated. We have made little if any progress on inflation. There is little if any reason to expect a large slowdown going forward.

Core PCE at an annual rate:

1 month: 7.1%

3 months: 4.7%

6 months: 5.1%

12 months: 4.7% pic.twitter.com/aCA1341MQd— Jason Furman (@jasonfurman) February 24, 2023

Furman’s numbers are accurate, of course. But is all this gloom really justified?

In the Long Run

If you’ve read any of my recent articles, you’ve probably noticed by now that I’m partial to the view of inflation advanced by John Maynard Keynes and his closest followers (most importantly Joan Robinson and Richard Kahn). For them, the key long-run driver of the price level is the level of wages relative to labor productivity.

The logic is straightforward: the level of wages is the most important single determinant of both the supply of and the demand for goods and services. It’s the central influence on supply because labor accounts for the bulk of production costs. And it’s the central influence on demand because wages are the primary source of the public’s spending power.

If wage growth accelerates faster than productivity, production costs go up, which induces firms to raise their prices. That increased wage income, crucially, then makes it possible for the public to pay the higher prices without cutting back on the real quantity of output they purchase. If it weren’t for the increase in nominal wage income, the rise in prices would represent a fall in real income for most people, which would reduce the flow of real purchases, depress the demand for labor, and soon enough bring a halt to the wage acceleration — and that would end the price acceleration, too. That’s why wage growth is so important in sustaining the inflation process.

When you look at things from this angle, the upshot is that any acceleration or deceleration of price inflation is unlikely to last very long unless it’s mirrored by an acceleration or deceleration of labor costs. This was the meaning of Robinson’s striking statement from 1938, which I quoted in an article last month, that “the essence of inflation is a rapid and continuous rise of money wages. Without rising money wages, inflation cannot occur, and whatever starts a violent rise in money wages starts inflation.”

The difficulty when we try to apply this analysis to an understanding of inflation on a month-by-month, quarter-by-quarter basis, is that the nexus between labor costs and inflation — though very tight in the “long” run — is looser and more elastic in the “short” run, because at each link in the chain of causation there’s always some short-term wiggle room. For example, if prices accelerate, nominal wage growth must ultimately accelerate, too, in order for the volume of real household purchases to be sustained; but that requirement can be temporarily relaxed if households dip into their savings. Similarly, if wage costs accelerate, prices must eventually accelerate, too; but that outcome can be temporarily forestalled if the share of income going to profits declines.

In all such scenarios, though, the important point is that the wiggle room is always limited and temporary: households that dip into their savings to maintain their monthly spending will eventually run out of savings to dip into. A declining share of income going to profits can go on for a while, but eventually profit will fall to a point where firms stop investing, likely sparking a recession.

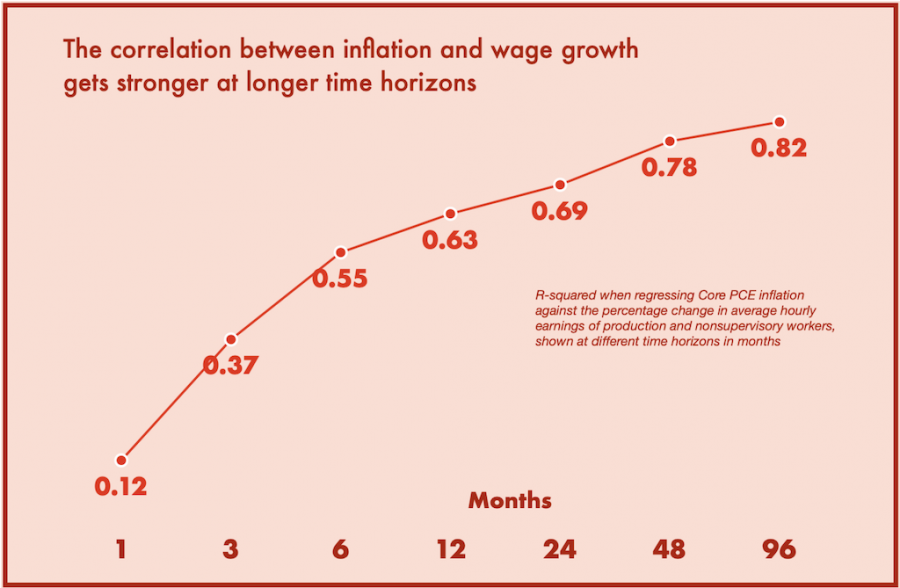

In the long run, therefore, inflation and labor costs always evolve in tandem. Exactly what “the long run” means here can be seen by looking at the strength of the correlation between inflation and wage growth at different time horizons. The chart below displays that relationship, using Core PCE as the measure of inflation (the Fed’s preferred measure) and the growth rate of average hourly earnings of production and nonsupervisory workers (who account for about 80 percent of employees) as the measure of wage growth.

If you correlate the rate of change of these two variables at a one-month frequency, the R-squared — the percentage of the variance of one variable that’s explained by the variance of the other variable — is only 0.12. But if you look at a three-month horizon, R-squared rises to 0.37. Over a frequency of a year, the relationship gets a lot stronger, 0.63, and it gets very strong, 0.69, at a three-year horizon. At a four-year horizon the R-squared rises to 0.78.

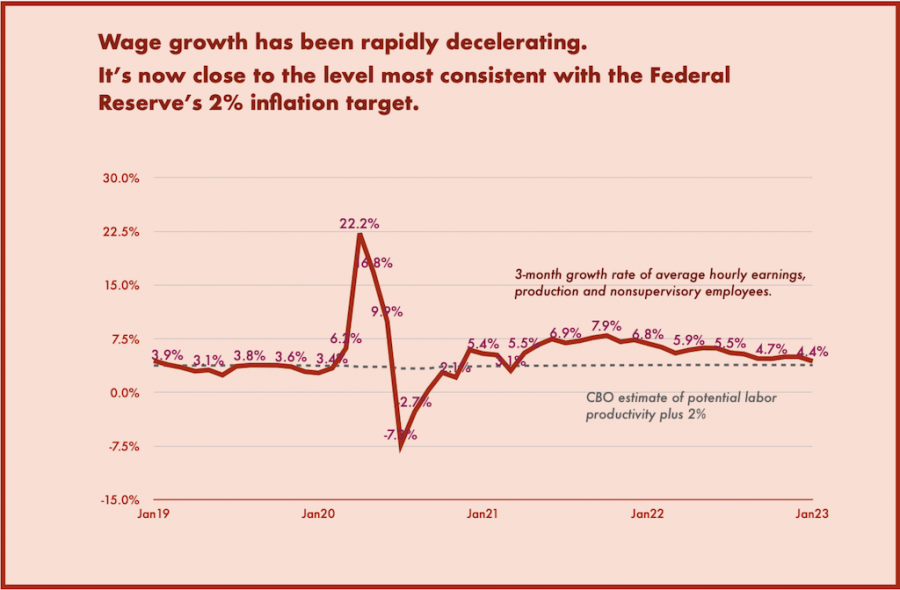

And that’s good news for anyone yearning for lower inflation, because it turns out that wage growth has experienced an extraordinary deceleration over the past year.

The chart below plots the three-month growth rate of nonsupervisory hourly wages against the hypothetical rate that could be considered most compatible with the Fed’s 2% inflation target — namely, the Congressional Budget Office’s estimate of trend productivity growth plus 2%.

By this measure, the deceleration of wage growth has been truly remarkable. In fact, since the massive disinflation engineered by former Fed chair Paul Volcker in the early 1980s, only three months have seen larger declines in the twelve-month wage growth rate (compared to the preceding twelve months) than what we saw last month. (And two of the three were statistical anomalies associated with the momentary collapse of employment during the spring 2020 pandemic lockdowns.)

To call an economy “very overheated,” as Furman did last week, when it’s experiencing such breakneck wage deceleration, is wrong practically by definition. The truth is that the most important underlying source of inflation is steadily dwindling, and it’s only a matter of time before it starts fully showing up in the data.