Choose Class War, Not Boomer Resentment

The generational warfare promoted by centrists and the Right, who have long been desperate to cut and privatize Social Security, is a fool’s solution to what ails the system. Taxing the rich is the answer.

“Total boomer luxury communism” is the Right’s latest attempt to convince younger Americans to slash their own future benefits under the guise of sticking it to older generations. (John Taggart / Bloomberg via Getty Images)

A specter is haunting the United States — the specter of “total boomer luxury communism.” Or at least that’s what conservative pundits want younger generations to think.

Conservative writer Russ Greene coined the term “Total Boomer Luxury Communism” (TBLC) in July 2025 as a cynical riff on the utopian left’s vision of a post-scarcity “fully automated luxury communism.” Greene elaborated on the TBLC idea in a December essay in the American Mind, one of the house organs of the Claremont Institute.

Founded in 1979 as a quixotic fusion of Barry Goldwater’s free-market fundamentalism and Leo Strauss’s conservatism, Claremont has become one of the most influential institutional champions of Trumpian “national conservatism.” When parts of the Right questioned Donald Trump’s conservative bona fides in 2016, the institute published Michael Anton’s viral essay, “The Flight 93 Election,” which urged conservatives to “charge the cockpit” — that is, vote for Trump — or “die.”

In return, Trump stocked his administration with Claremont alumni — the self-styled “Claremonsters” — across both terms. The institute’s largest donor, hedge fund manager Thomas Klingenstein, believes that conservatism is locked in a “cold civil war” against “woke communism” and “social justice.” As Vice President J. D. Vance recently quipped, Claremont is “the only group maybe in California that makes me seem like a reasonable moderate.”

Greene is CrossFit’s former director of government relations and the current head of the Prime Mover Institute, an energy-industry group that has called for repealing the Environmental Protection Agency’s Carbon Pollution Standards.

“The essence of TBLC,” Greene writes, “is that it redistributes wealth from younger families and workers to seniors, who are on average much richer.” The result, he argues, is a cohort of retirees living in a “Marxist paradise of hunting in the morning, fishing in the afternoon, rearing cattle in the evening, and criticizing after dinner.”

This “generational injustice,” Greene claims, is “driving every aspect of American decline — from skyrocketing national debt and the erosion of the defense industrial base to the despair of young people.” His remedy is to “radically overhaul America’s entitlement regime” by cutting Social Security and Medicare, even if it forces recipients — whom he calls “welfare queens” — back into the workforce or compels them to sell their homes.

Greene’s TBLC framework has been endorsed and amplified by figures affiliated with a range of billionaire-backed think tanks — including the conservative Capital Research Center, the neoliberal Institute for Progress, and the right-libertarian Cato Institute and Reason Foundation — as well as by centrist blogger Matt Yglesias, white supremacist Jordan Lasker, and conservative columnist George Will.

Taken at face value, the timing of the TBLC discourse might seem strange. After all, the oldest boomers are turning eighty years old this year, and millennials are now the largest generation. That’s because the real motivation behind the emergence of the TBLC argument is the looming exhaustion of the Social Security trust fund in 2032, which will provide opponents of the old-age safety net with their best opportunity in decades to cut it.

“Total boomer luxury communism” is the Right’s latest attempt to convince younger Americans to slash their own future benefits under the guise of sticking it to older generations.

It’s manufactured generational warfare dressed up as legitimate class conflict, meant to distract from the cross-generational economic inequality — and the policies that have fueled it — at the root of younger Americans’ economic anxieties.

A Leninist Strategy for Privatization

From its inception as part of Franklin D. Roosevelt’s New Deal, Social Security has faced conservative opposition. Business groups such as the US Chamber of Commerce, the National Association of Manufacturers (NAM), and the Du Pont–backed American Liberty League lobbied aggressively against government-provided old-age pensions. Testifying before Congress, NAM’s Noel Sargent argued that Social Security would “increase dependency and indigency” while eroding the “individual energy and efficiency” of the elderly to “take care of themselves.”

Republican James W. Wadsworth Jr struck a more apocalyptic tone, warning that Social Security “opens the door and invites the entrance into the political field of a power so vast, so powerful as to threaten the integrity of our institutions and so pull the pillars of the temple down upon the heads of our descendants.”

Medicare received a similar reception from the Right when enacted under Lyndon Johnson. Barry Goldwater, Johnson’s Republican challenger in 1964, made a proto-TBLC case against Medicare, quipping, “Having given our pensioners their medical care in kind, why not food baskets, why not public housing accommodations, why not vacation resorts, why not a ration of cigarettes for those who smoke and of beer for those who drink?”

Most famously, Ronald Reagan committed his opposition to Medicare to vinyl. He predicted that if Medicare became law, “you and I are going to spend our sunset years telling our children, and our children’s children, what it once was like in America when men were free.”

Throughout the 1960s and ’70s, Reagan talked up Social Security privatization, only to distance himself from the idea during his 1980 presidential campaign. Once in office, however, he proposed a roughly 10 percent reduction in future Social Security outlays. The Reagan era ultimately produced the Greenspan Commission and the Social Security Amendments of 1983, which raised the full-benefit retirement age from sixty-five to sixty-seven, among other changes.

The Right’s failure to impose deeper cuts on the old-age safety net during the Reagan era led the Heritage Foundation’s Stuart Butler and Peter Germanis to call for what they bluntly described as a “Leninist strategy” to privatize Social Security. The obstacle, they conceded, was simple: the public liked the program. Conservatives, therefore, needed to be “ready for the next crisis in Social Security,” which “may be further away than many people believe.”

Preparing to exploit that crisis moment, they wrote, would require mobilizing “the banks, insurance companies, and other institutions that will gain” from privatization while waging “guerrilla warfare against both the current Social Security system and the coalition that supports it.”

Foreshadowing TBLC and other generation-based privatization appeals, Butler and Germanis argued that “the young are the most obvious constituency for reform and a natural ally for the private alternative,” provided they could be convinced through a “comprehensive program of economic education” that “the prospects for a reasonable return on one’s ‘contribution’ [will] continue to fade.”

Boomers as Victims

In the decades that followed, a seemingly endless series of “deficit hawk” organizations — including the Committee for a Responsible Federal Budget, Americans for Generational Equity, the Concord Coalition, Lead . . . or Leave, Third Millennium, The Can Kicks Back, and Fix the Debt — worked to convince younger Americans of the need for radical cuts to Social Security and Medicare. Each was backed by pro-privatization investment banker Peter G. Peterson, along with a predictable coalition drawn from business, finance, and conservative think tanks.

Drawing on the dubious writings of William Strauss and Neil Howe, these organizations understood that framing economic issues generationally — rather than in terms of class or other categories — was crucial to their success. As Republican Senator David Durenberger, chair of Americans for Generational Equity (AGE), put it, “The more America’s leaders talk about and think in terms of generational equity, the more effective AGE will be in its education program, and the better chance we will have of making the difference on crucial legislative issues.”

While the generations in question changed, the message these organizations delivered to the youth of the day remained the same: retirees are greedy, Social Security and Medicare won’t be there for you, and it’s time to cut and privatize.

Strauss and Howe’s early work cast baby boomers as the victims of the Silent Generation’s profligacy, and early pro-privatization groups claimed to speak on their behalf. As AGE’s Phillip Longman wrote in the New York Times, “The Baby Boomers as a whole are far from ‘upwardly mobile’. . . . A declining proportion of younger Americans own their own homes, and those who do are typically encumbered by unprecedented mortgage payments.” The problem, according to Longman, was that “Baby Boomers are paying an unprecedented share of their income to support the current older generation.”

With the backing of Peterson, Exxon, and General Motors, among other corporate heavy-hitters, AGE garnered widespread media coverage throughout the 1980s. In the 1988 presidential primaries, AGE endorsed the two candidates — former Republican governor Pete du Pont and televangelist Pat Robertson — willing to call for the privatization of Social Security. But only a few years later, AGE collapsed after investigations into Durenberger’s use of the organization to boost his own reelection campaign.

AGE wasn’t alone in marshaling empathy for the boomers for conservative ends.

The Democratic Leadership Council (DLC), a corporate-funded “New Democrat” organization, invoked “the question of equity among generations” as it lobbied for both cuts to and partial privatization of Social Security. The DLC argued that “millions of retirees, without regard to their need, reap windfalls from Social Security beyond the interest-adjusted value of their tax contributions into the system” at the expense of “millions of baby boomers” who “have paid steep payroll taxes for two decades and are struggling with their parents’ retirement needs even as they worry about their own.”

But despite being saddled with Reagan’s cuts to Social Security, boomers resisted entreaties to turn against the program. So opponents of Social Security and Medicare shifted course, pinning their hopes on Generation X.

Boomers as Villains

As the 1990s began, Strauss and Howe updated their generational theory for a younger audience. In 13th Gen, they now argued that boomers and previous generations had “push[ed] every policy lever conceivable — tax codes, entitlements, public debt, unfunded liabilities, labor laws, hiring practices — to tilt the economic playing field away from the young and towards the old.”

13th Gen reinforced this narrative with a series of heavy-handed political cartoons: a tidal wave of national debt looming over twentysomethings (“HONEY, I SOAKED THE KIDS”); lunching boomers debating the purchase of a “second Beemer” while complaining about the Gen X waitstaff; and an elderly couple tossing the keys to a Cadillac — license plate “I-URND-IT” — to a teenage country-club valet without dropping a dime into his “COLLEGE FUND” tip jar.

A new target generation meant new organizations, too. With backing from Peterson and Ross Perot, recent college grads Rob Nelson and Jon Cowan founded Lead . . . or Leave (LOL) in 1992. LOL billed itself as “the largest grassroots college/twentysomething organization in the country.” In their manifesto, Revolution X, Nelson and Cowan called for cutting Social Security benefits for current retirees and transitioning future generations to mandatory private accounts.

Though Nelson and Cowan appeared on ABC’s Nightline, CBS This Morning, and CNN, and were profiled by dozens of print outlets, LOL proved to be a house of cards. Its vaunted membership numbers counted every student at any college where it had a single member. Though it managed to wrangle five hundred people for a “Dis the Deficit” protest on capitol hill, LOL’s other high-profile plans — including a promised “Rock the Debt” concert and 1996 election protests at which Gen Xers would burn their Social Security cards — never materialized. LOL soon folded.

LOL was succeeded by Third Millennium (TM). With funding from Peterson, the Prudential Foundation, Merrill Lynch, and several business groups, Third Millennium marketed itself as a “post-partisan” Gen X version of Students for a Democratic Society, complete with a self-important “Third Millennium Declaration” that labeled Social Security “a generational scam — fiscally unsound and generationally inequitable.”

Like AGE and LOL, the media and sympathetic politicians lavished attention on TM. Its leaders — including Meredith Bagby, Richard Thau, and Maya MacGuineas — appeared on NBC’s The Today Show and CBS This Morning and testified before Congress. Warning of “generational warfare,” TM called for the privatization of Social Security. It organized a “Call Your Grandma” campaign urging young people to persuade their grandparents to oppose the addition of prescription drug coverage to Medicare and instead support “comprehensive Medicare reform that relies on a public-private partnership of competition and choice.”

TM also bought ads on MTV as part of the “Coalition for Change.” One commercial featured a young woman lamenting, “At this rate, I’ll be spending my whole life paying off the bills run up by our parents and grandparents. Without change, programs like Medicare won’t have any money left by the time I retire.”

TM’s most successful stunt was hiring Republican pollster Frank Luntz to gauge young people’s attitudes toward Social Security. Rather than field a traditional survey, TM’s board pushed for the inclusion of an unrelated question about UFOs — a setup that allowed them to disingenuously pit young people’s confidence in Social Security against their belief in life from outer space.

In an era when major publications were dubbing Social Security a “Ponzi scheme,” referring to seniors as “greedy geezers,” and giving Peterson cover space to argue for replacing Social Security with “mandatory” private savings, the press eagerly amplified the resulting talking point. It appeared in some five hundred news stories and reached the White House. In a 1998 speech at the University of Illinois, President Bill Clinton quipped “that young people in their twenties think it’s more likely that they will see UFOs than that they will ever collect Social Security.”

“If we had done nothing else, that was our signal achievement,” TM’s Thau recalled to journalist Eric Laursen, “perhaps more important to the culture and the Social Security discussion than anything else we did.” In fact, the talking point hinged on a misleading juxtaposition of two unrelated questions. When asked directly whether UFOs were more likely than collecting Social Security, young Americans chose Social Security by a two-to-one margin.

Despite the efforts of Wall Street and groups like LOL and TM, the Clinton-era push to cut or privatize Social Security ran headlong into political reality.

In 1995, Democratic Senator Bob Kerrey and Republican Senator Alan Simpson proposed raising the retirement age to seventy and partially privatizing Social Security. The plan made waves in the press — Kerrey even cited TM’s UFO poll in defending it — but it went nowhere in Congress.

Following Clinton’s reelection in 1996, the DLC pushed him to pursue a “fundamental restructuring” of Social Security and Medicare by bringing both “into marketplace.” Will Marshall, the president of the DLC-affiliated Progressive Policy Institute (PPI), called for a “grand bargain” based around “personal accounts [that] would refashion Social Security from a system of wealth transfer into one that also promotes individual wealth creation and broader ownership.”

In late 1997, Clinton met secretly with House GOP leader Newt Gingrich and Ways and Means chair Bill Archer to hammer out a plan to partially privatize Social Security and Medicare. “I’m prepared to take the political heat to provide political cover for the Republicans,” Clinton assured Archer. For Social Security, the outlines of the deal included a hike in the retirement age and the diversion of a portion of payroll tax dollars into private accounts. Fortunately, the revelation of Clinton’s affair with White House intern Monica Lewinsky derailed the talks.

As the scandal exploded, Clinton picked up a proposal made by former Social Security Administration (SSA) commissioner Robert Ball and other members of the mid-’90s Advisory Council on Social Security for the government, rather than individuals, to invest payroll taxes in higher-yield equity index funds. The Advisory Council argued it would be “possible to maintain Social Security benefits for all income groups of workers, greatly improving the money’s worth for younger workers, without incurring the risks that could accompany individual investment.”

An independent federal fund could offer low administrative costs and socialized risk — in sharp contrast to individual private accounts, whose fees would vastly outstrip Social Security’s minuscule administrative costs and whose holders would face the danger of seeing their savings wiped out by a market downturn just as they were about to retire.

Clinton proposed investing approximately 15 percent of Social Security’s surplus into index funds. Experts like Robert Reischauer, Alan Blinder, Robert Greenstein, and Henry Aaron endorsed the plan. As Aaron told the Senate Budget Committee in 1999, “Because administrative costs would be smaller, investment of part of the trust funds in equities would yield higher returns than individual accounts, while protecting beneficiaries from the risks they would bear under a system of individual accounts.”

Clinton also proposed Universal Savings Accounts, a supplementary program outside of Social Security that would automatically deposit $300 per year into retirement accounts for lower- and middle-income workers, with the government matching additional contributions.

Some progressive Democrats were understandably skeptical of the plan, and the public’s reaction was lukewarm, at best. But Federal Reserve Chairman Alan Greenspan, congressional Republicans, and other conservatives ultimately sank it. They saw the federal fund as socialistic and the external individual accounts as insufficient. For the Right, individual private accounts within Social Security were the only acceptable solution.

The Right’s best shot at privatization came during President George W. Bush’s administration. Bush spent the “political capital” he claimed to have earned from his narrow reelection in 2004 on a plan to partially privatize Social Security, which he claimed would be “a better deal for younger workers” who’d been “stuck with an enormous tab” by baby boomers like him.

Bush’s plan was boosted not merely by conservative think tanks like Cato — whose Michael Tanner told Congress that “more privatization is better than less” because “you don’t cut out half a cancer” — but also by the Peterson-backed Committee for a Responsible Federal Budget (CRFB) led by former TM board member MacGuineas.

The problem was that, as one account noted, “the more the President talked about Social Security, the more support for his plan declined,” and Bush ultimately dropped the plan.

Pro-privatization forces were more successful with Medicare. The 1997 budget bill passed by Republicans in Congress and signed by President Clinton included Medicare+Choice, which opened Medicare to private plans. Medicare+Choice was expanded and renamed Medicare Advantage as part of the Bush-era legislation that created Medicare’s prescription drug coverage.

Manufacturing Millennial Outrage

Though the cost of the Bush tax cuts far exceeded the long-run Social Security shortfall, and Vice President Dick Cheney famously declared that “deficits don’t matter,” Republicans predictably rediscovered their fiscal hawkery once Democrat Barack Obama entered the White House.

Taking that concern at face value, Obama foolishly pivoted to deficit reduction in 2010, even as the economy was still reeling from the Great Recession, and appointed the National Commission on Fiscal Responsibility and Reform — better known as the Simpson-Bowles commission, after its two chairs, the aforementioned Alan Simpson and President Clinton’s former chief of staff, Erskine Bowles.

From the outset, the Simpson-Bowles commission tilted toward a conservative vision of deficit reduction. It proposed cutting top corporate and individual income tax rates even as it called for cuts to Social Security, including raising the retirement age to sixty-nine and shifting to a slower cost-of-living adjustment that understates the inflation faced by retirees. The result was a roughly 2:1 ratio of spending cuts to new revenue.

At the same time, Rep. Paul Ryan rolled out a series of Republican budget blueprints that would have sharply reduced taxes on corporations and high earners by cutting individual rates, scrapping the corporate income tax in favor of a border-adjusted consumption tax, and eliminating taxes on investment income and estates. Ryan paired those tax cuts with proposals to privatize Medicare and shift Social Security toward individual accounts.

This Obama-era push for cuts to Medicare and Social Security brought with it a new wave of Peterson-backed groups, along with yet another downward shift in the target generation.

The most prominent of the new Peterson-backed groups, Fix the Debt (FTD), enlisted Simpson and Bowles as its cochairs. CRFB functioned as its de facto parent organization, and its president, MacGuineas, also headed FTD. While Bowles — by then a Morgan Stanley board member — lent the effort a bipartisan veneer, the eighty-six CEOs on its Fiscal Leadership Council were overwhelmingly Republican donors.

FTD’s public relations blitz stumbled early when one of its CEO backers, Goldman Sachs chief Lloyd Blankfein, told CBS in November 2012, “You’re going to have to undoubtedly do something to lower people’s expectations [about] entitlements and what people think that they’re going to get, because it’s not going to happen. They’re not going to get it.” The remark triggered a wave of reporting on the outsize compensation and retirement packages enjoyed by Blankfein and other executives backing FTD, as well as their behind-the-scenes lobbying to shield their own tax preferences from any deficit deal.

Shifting onto firmer ground, FTD began airing commercials in December that leaned heavily on the idea that the national debt represented an albatross around the necks of younger generations. In one, a teacher laments, “I would love for everything to start getting resolved now so that I can tell my children and the children that I teach and not be lying to them when I say to them that there is a bright future and you can do anything that you want to do.”

FTD also launched a youth affiliate, The Can Kicks Back (TCKB), to gin up generational outrage. Billed as a “millennial-driven campaign to solve America’s fiscal crisis,” TCKB’s stated goal was to “organize over 100,000 young people” to demand “fiscal sustainability and generational equity.” Although TCKB’s staff consisted largely of people in their twenties and thirties, its advisory board included both Simpson and Bowles as well as LOL’s Cowan, who was now serving as the president of Third Way, a centrist Democrat think tank with deep Wall Street ties.

Sandwiched between Occupy Wall Street and Bernie Sanders’s youth–powered 2016 campaign, TCKB pressed generational conflict as a substitute for class politics more forcefully than any of its predecessors. Through its “Swindled” project, TCKB warned of an “economic crisis” caused by “inequality beyond anything we’ve ever seen before.” This was “not the gap between the rich and the poor,” according to TCKB. Instead, it was “the one between the young and the old,” which was “threatening for the first time in our history to leave one generation worse off than their parents and grandparents.”

TCKB’s policy prescriptions were predictable. It called for a “grand generational bargain” built around “reforming the tax code” and “slowing the growth of entitlement spending.” Unsurprisingly, given its advisory board, it endorsed the Simpson-Bowles plan. TCKB heaped praise on Paul Ryan’s budget, ranking it first in its March Madness–style “Budget Madness” bracket and applauding Ryan’s “courage and leadership on budget issues.” It also proposed the Intergenerational Financial Obligations Reform (INFORM) Act, which sought to codify inherently inaccurate and misleading “generational accounting” as an alternative to the federal government’s traditional income-based distributional analyses.

In addition to TCKB, Peterson poured nearly half a billion dollars between 2007 and 2011 into a range of initiatives aimed at convincing Americans — especially younger ones — of the need to cut or privatize Social Security and Medicare.

Partnering with MTV’s campus network, mtvU, he launched the Indebted campaign, whose website featured a “Debt Ski” video game and deficit-themed pop-up videos for songs by artists like Kanye West, Lily Allen, and Fall Out Boy. Like TCKB, Indebted warned that government deficits were dooming young people “to be the first generation that won’t enjoy the same growth in standard of living as their parents.”

Reaching for an even younger audience, Peterson also funded an “Understanding Fiscal Responsibility” curriculum through Columbia University’s Teachers College. Six of its fifteen lessons focused on Social Security and Medicare, while just one zeroed in on taxation. It was distributed for free to high schools nationwide.

Few of Peterson’s efforts had the desired effect.

Like LOL and TM, TCKB sought to project the image of a mass movement. It brought its “AmeriCAN” mascot — literally “a giant can character” meant to “represent the young Americans who are kicking back to reclaim their future” — on a “Generational Equity Tour” of college campuses, where organizers hoped to launch local chapters and dramatize millennial concern about the “growing economic inequality between younger and older Americans as a result of current fiscal policy” by collecting aluminum cans from students.

The tour did not go as planned.

TCKB was exposed for planting identical, ghostwritten op-eds in college newspapers nationwide. Critical editorials in the Georgetown and University of Virginia student papers accusing TCKB of being an “astroturfed” campaign “misrepresenting” itself to students. A leaked internal email revealed TCKB staffers lamenting, “We generated 800 cans through our national tour at a cost of about $3,000 per can.”

TCKB’s only genuinely viral moment came when it persuaded the eighty-one-year-old Simpson to dance “Gangnam Style” in a video alongside “AmeriCAN.” But the video gained attention more for its absurdity — with Simpson telling the press that he “made a perfect ass” out of himself — than for its message, perhaps because it consisted of Simpson scolding youth to “stop Instagramming your breakfast and tweeting your first world problems” and instead “start using those precious social media skills to go out and sign people up on this baby,” otherwise “these old coots will clean out the Treasury before you get there.”

By early 2014, TCKB’s funding had dried up, and one member of its dwindling staff privately conceded that “Fix the Debt is increasingly seen (I think in a lot of ways justifiably) as a mouthpiece for corporate America, and particularly Wall Street.”

The Obama-era push for a deficit deal collapsed as well. Despite proposals calling for anywhere from a 2:1 to a 6:1 ratio of spending cuts to revenue increases, Republicans balked at any tax hikes, while pressure from progressives such as Sanders and Elizabeth Warren pushed Obama to retreat from cutting Social Security.

Phony Generational War

With the TBLC discourse, Greene and like-minded conservatives appear to view the Social Security trust fund’s projected depletion as the “next crisis” foretold by Butler and Germanis — a moment to force through cuts or privatization that had previously proved politically toxic, despite the efforts of AGE, LOL, TM, TCKB, and the veritable alphabet soup of other groups.

Indeed, Greene’s playbook reads like a modernized version of Butler and Germanis’s “Leninist strategy.” As Greene has written:

To terminate TBLC we need to:

Raise awareness of mass generational injustice.

Align Wall Street, the defense industrial complex, corporate America, and the media against TBLC (the alternative is tax hikes, cuts to discretionary spending and a debt crisis).

Form a counter-AARP.

Greene sees the growing number of articles “aligned“ with his TBLC framework as proof that the strategy is working. While its ultimate success remains to be seen, there’s no doubt that an effort to paint boomers as the new “greedy geezers” is gaining traction.

The key to the TBLC narrative is the idea that, as Greene has put it, baby boomers are “the wealthiest, most privileged generation in America,” consisting of “retired millionaires [with] country club lifestyles.” Yet this impression rests on misleading data that simultaneously exaggerates the wealth and understates the needs of the average boomer, while ignoring the deeper inequalities within and across generations that point toward income-based redistribution rather than generational demagoguery.

Most articles that emphasize baby boomers’ wealth rely on measures of mean wealth by generation or each generation’s share of total wealth. Because these measures ignore inequality within generations, they can be misleading. If Jeff Bezos, a baby boomer, were to transfer his wealth to Mark Zuckerberg, a millennial, both metrics would suddenly make boomers appear poorer and millennials richer — even though nothing about the actual economic circumstances of either generation would have changed.

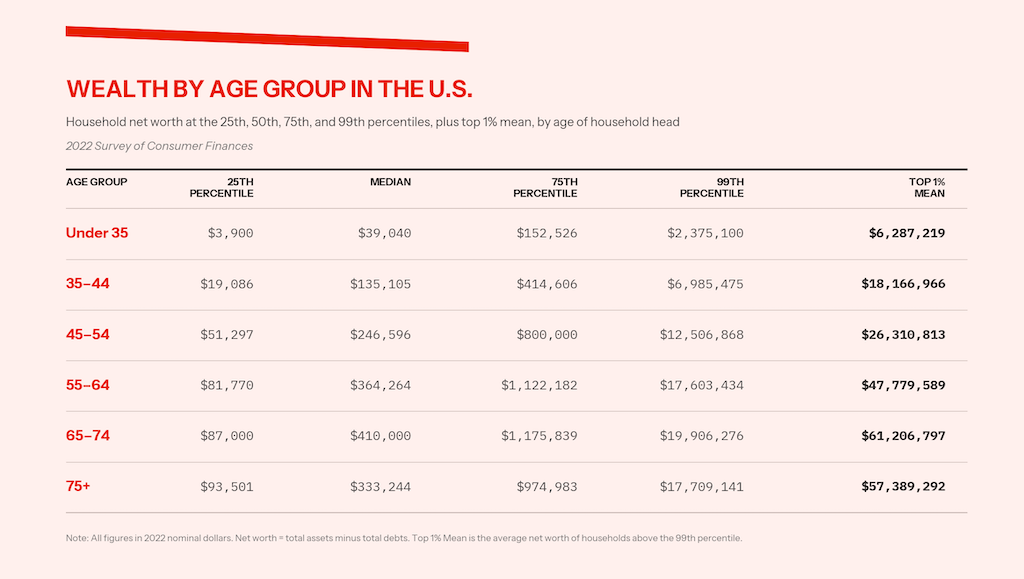

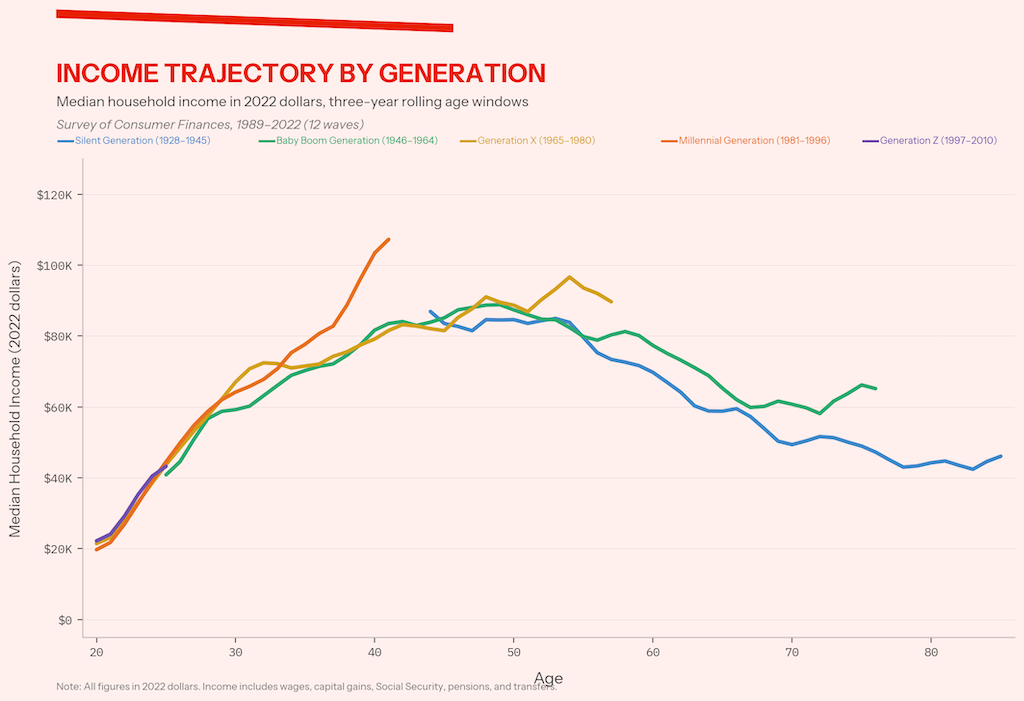

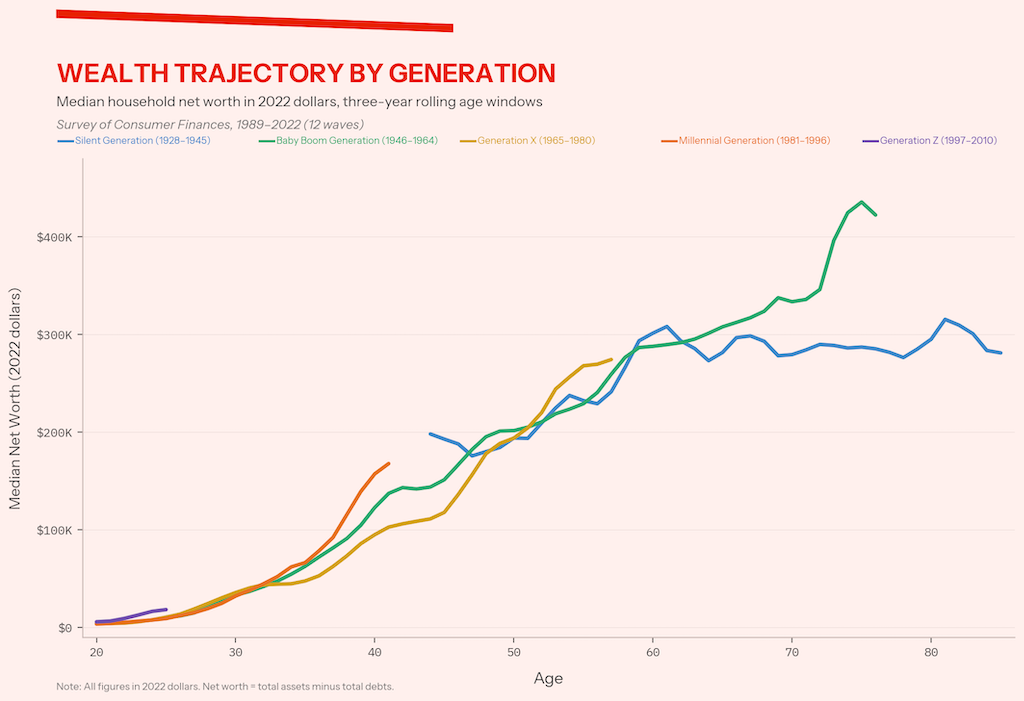

Looking at wealth by percentile using the Federal Reserve’s Survey of Consumer Finances (SCF) provides a much more realistic picture of each age group’s net worth.

Older households are wealthier. That’s no surprise, given that they’ve had longer to save.

But wealth inequality within age groups swamps wealth inequality between them. The median household aged sixty-five to seventy-four has three times the wealth of the median household aged thirty-five to forty-four. But the 99th percentile of households aged thirty-five to forty-four has fifty times the wealth of that group’s median, and the top 1 percent of households aged thirty-five to forty-four average 134 times the median.

The 99th percentile of households aged sixty-five to seventy-four holds forty-seven times their age group’s median, while the top 1 percent averages 147 times the median. The lack of wealth at the bottom is just as consistent. The 25th percentile never exceeds half the overall median in any age group.

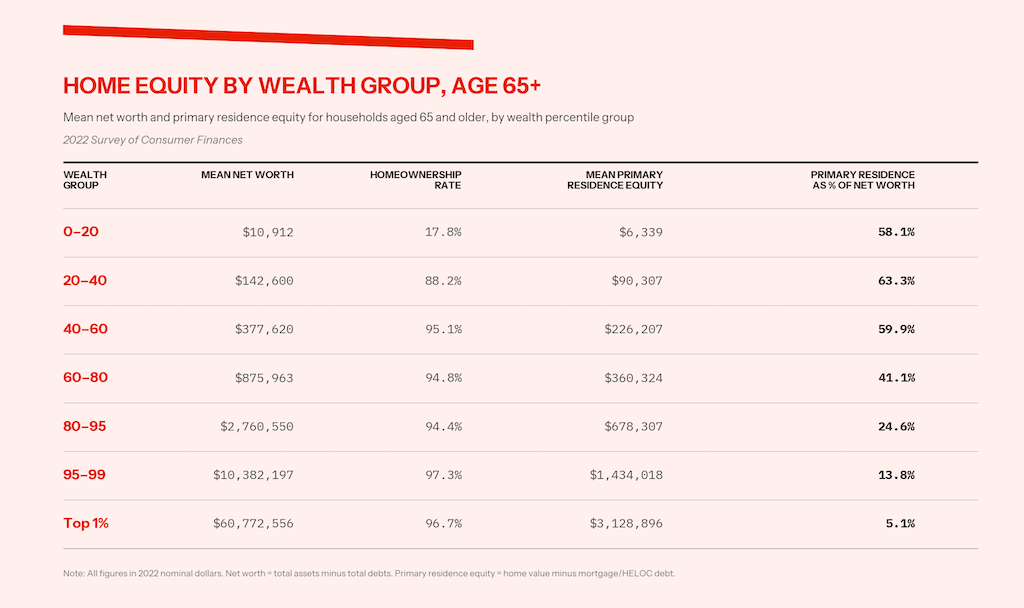

Making matters more complicated: even though older households are wealthier, on average, for most households over sixty-five, that wealth isn’t liquid. Instead, it’s equity in their primary residence.

Nearly 60 percent of the roughly $375,000 in wealth held by the middle wealth quintile of over-sixty-five households is composed of home equity. For the bottom 60 percent of elderly households, the primary residence accounts for most of their net worth. It’s only within the top fifth of households over sixty-five that a significant portion of wealth comes from something other than their primary residence.

Non-white older households are especially likely to have their wealth tied up in their home they occupy. Moreover, the percentage of homeowners over sixty-five with a mortgage has nearly doubled, from 21 percent to 39 percent, since 1989.

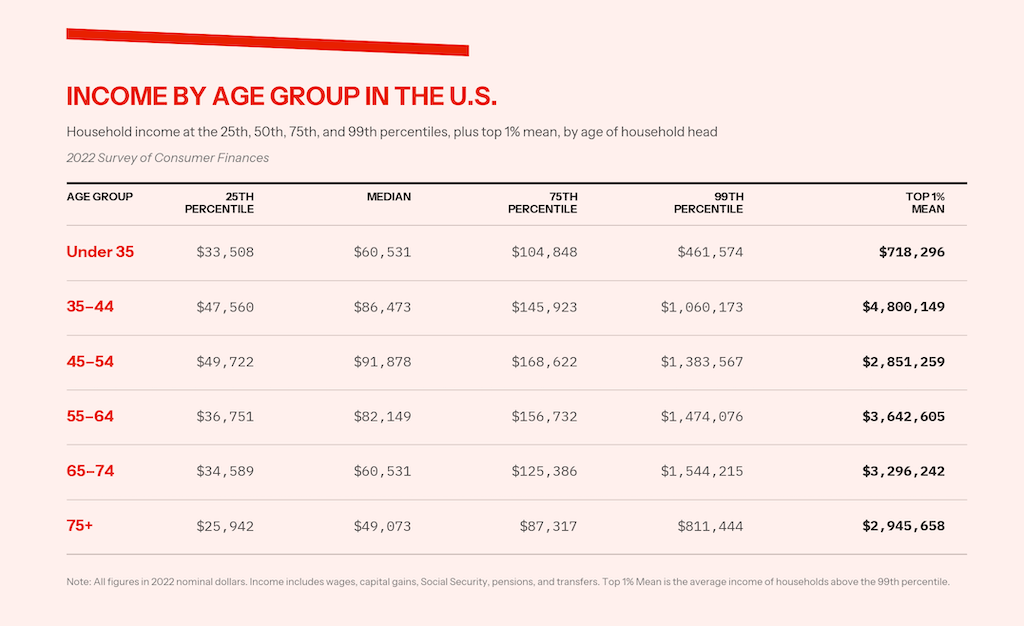

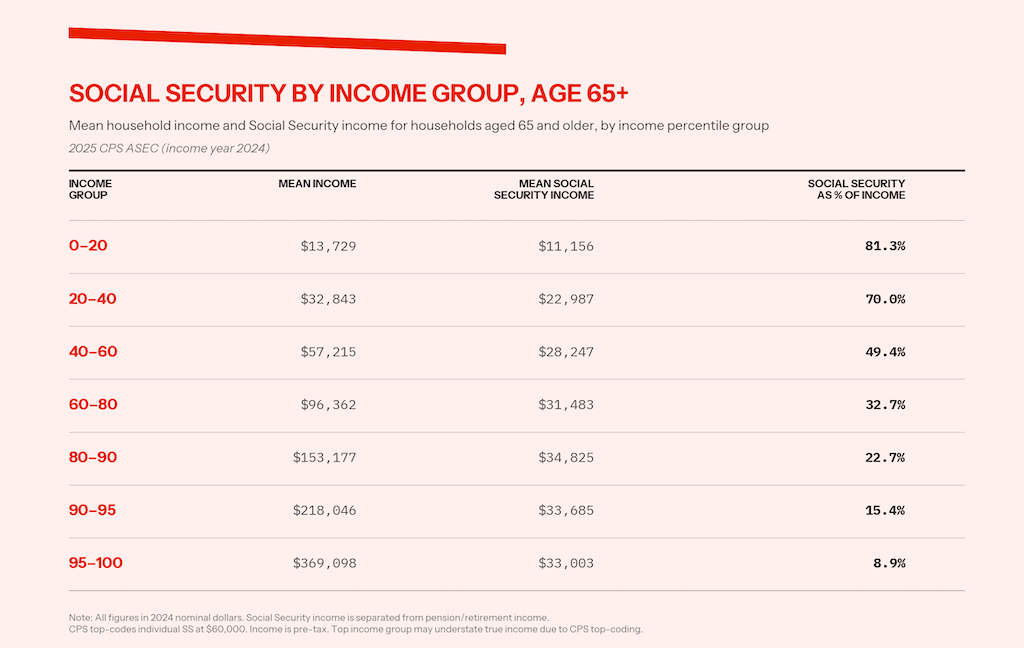

Things look even worse for older households when it comes to income. SCF data is pre-tax, but includes wage income, pensions, Social Security, and other cash transfers.

Households over seventy-five have the lowest household income of approximately $50,000. The sixty-five to seventy-four and under thirty-five age groups are next, both making about $60,000 per year. Individual, rather than household, income data from the census shows the same pattern.

Americans sixty-five and older have the lowest income — approximately $35,000, including Social Security — of any age group besides those between fifteen and twenty-five. This isn’t surprising, given that both age groups largely consist of people who are too young or too old to work. Transferring money from working-age adults to kids and the elderly is one of the main functions of all welfare states.

It’s also worth considering that the elderly — like lower-income people more broadly — face higher inflation rates. The “Elder Index,” published by the Gerontology Institute at the University of Massachusetts Boston, is a county-level estimate of the income older adults need to meet basic living expenses without relying on family support or means-tested public assistance.

Nationally, for a couple in good health, the index estimates annual costs of roughly $38,000 for homeowners without a mortgage, $47,000 for renters, and $52,000 for homeowners with a mortgage. Depending on the data source, between 25 and 45 percent of older households fall below those thresholds. As a result, about a third of midlife adults provide financial support to their parents, underscoring the reality that younger generations’ financial security is imperiled by older generations’ lack thereof.

Even if most elderly households aren’t rich now, that doesn’t settle the question of whether Gen X, millennials, and Gen Z are worse off than boomers were at similar ages. But historical SCF data allows for those comparisons.

While baby boomers fared better than the Silent Generation, younger generations have all done just as well as — or even better than — boomers. Younger households fare even better relative to boomers when including taxes and adjusting for falling household sizes.

There’s good reason not to be Pollyannaish about the economic fortunes of younger generations, however. While the SCF suggests that the median millennial household is wealthier than its boomer counterpart at the same age, studies using other surveys find that poor and middle-class millennials are worse off, while wealthy millennials are much better off, than comparable boomers.

Because these surveys are older than the SCF — and millennials have experienced the strongest wealth growth in recent years — they may paint an overly pessimistic picture of the median millennial today. Nonetheless, they underscore the importance of the within-generation inequality ignored by the TBLC discourse’s cross-generational focus. Indeed, by some measures, millennials are the most unequal generation in US history.

There’s also evidence that millennials are less likely to experience absolute upward mobility — that is, earn more than their parents in real terms — than any generation in modern US history. Moreover, home ownership rates for both millennials and Zoomers lag behind previous generations’ rates at similar ages, regardless of education level or income, thanks to the twin albatrosses of rising housing prices and student loan debt.

Ultimately, there’s little evidence to support the TBLC claim that boomer retirees are living in a “Marxist paradise.” More importantly, the worse off one believes Gen X, millennials, and Gen Z are compared to boomers, the more intergenerationally unjust the cuts to Social Security proposed by conservatives are.

Conservatives’ Generational Myths

As with earlier attempts to persuade younger generations to support cuts to old-age benefits, proponents of the TBLC narrative hope to create the impression that cutting Social Security would allow younger Americans to stick it to supposedly “greedy geezers.”

Last month, conservative Washington Post columnist Ramesh Ponnuru declared, “Don’t Save Social Security.” Echoing the TBLC discourse, Ponnuru argued that the program simply funnels money to already-well-off retirees — citing the common conservative talking point that a rich retired couple could receive $100,000 in benefits each year.

He also contended that Social Security is too generous to middle-income retirees, since “a middle-class worker who retires in the next decade will, on average, receive 47 percent more than the sum of what the person paid in taxes and the interest on that money,” while simultaneously being too stingy to poor ones, given that “even though Social Security paid out $1.6 trillion last year, around 6 percent of seniors still live in poverty.” His solution? Raise the retirement age and replace the current benefit formula with a flat payment set at 150% of the poverty line.

In mid-March, the CRFB’s MacGuineas appeared before Republican Ron Johnson’s Senate Finance Subcommittee on Fiscal Responsibility and Economic Growth. In her testimony, she claimed that “seniors are the richest” Americans, decried the “generational imbalance” of current spending, and warned of “generational resentment.”

Having previously coauthored a plan to cut and partially privatize Social Security, she called for “reforms” to old-age programs and proposed creating another Simpson-Bowles-style fiscal commission to enact them. Following her testimony, Johnson — who has called Social Security a “Ponzi scheme” and proposed privatizing it — posted a video of her remarks on social media, writing, “It is immoral what we are doing to our children and grandchildren.”

Critics thus portray Social Security as a system that is too generous to well-off retirees and too stingy to poor ones, while also being a great deal for boomers and a terrible deal for younger generations. Neither claim holds up to scrutiny.

Social Security is a progressive system designed to provide proportionally higher benefits to workers with lower earnings. Benefits are calculated using a formula that replaces 90 percent of the first $1,024 of a worker’s average monthly earnings, 32 percent of earnings between $1,024 and $6,172, and 15 percent above that level. As a result, lower-income workers receive benefits that replace a larger share of their preretirement income than higher earners.

Despite conservatives’ frequent invocation of couples collecting $100,000 per year in Social Security benefits, most retirees receive far more modest payments. The mean monthly retirement benefit is about $1,975, while the median is roughly $1,195. Just 13 percent of retirees receive more than $3,000 per month, and fewer than 3 percent receive over $4,000.

Among households over sixty-five, the middle quintile receives about $2,400 per month in Social Security benefits. For the bottom 80 percent of households, moreover, Social Security provides a substantial share of total income — a crucial consideration when evaluating any changes to benefits.

How many households actually receive $100,000 or more per year in Social Security benefits? Just two-tenths of 1 percent, according to Current Population Survey data. In fact, only about 5 percent of households receive $60,000 or more. That’s why proposals to establish an inflation-adjusted $100,000 benefit cap don’t save much in the short run but generate growing long-term savings by eroding the share of preretirement wages replaced by Social Security for both the rich and upper-middle class workers, since wages grow faster than inflation.

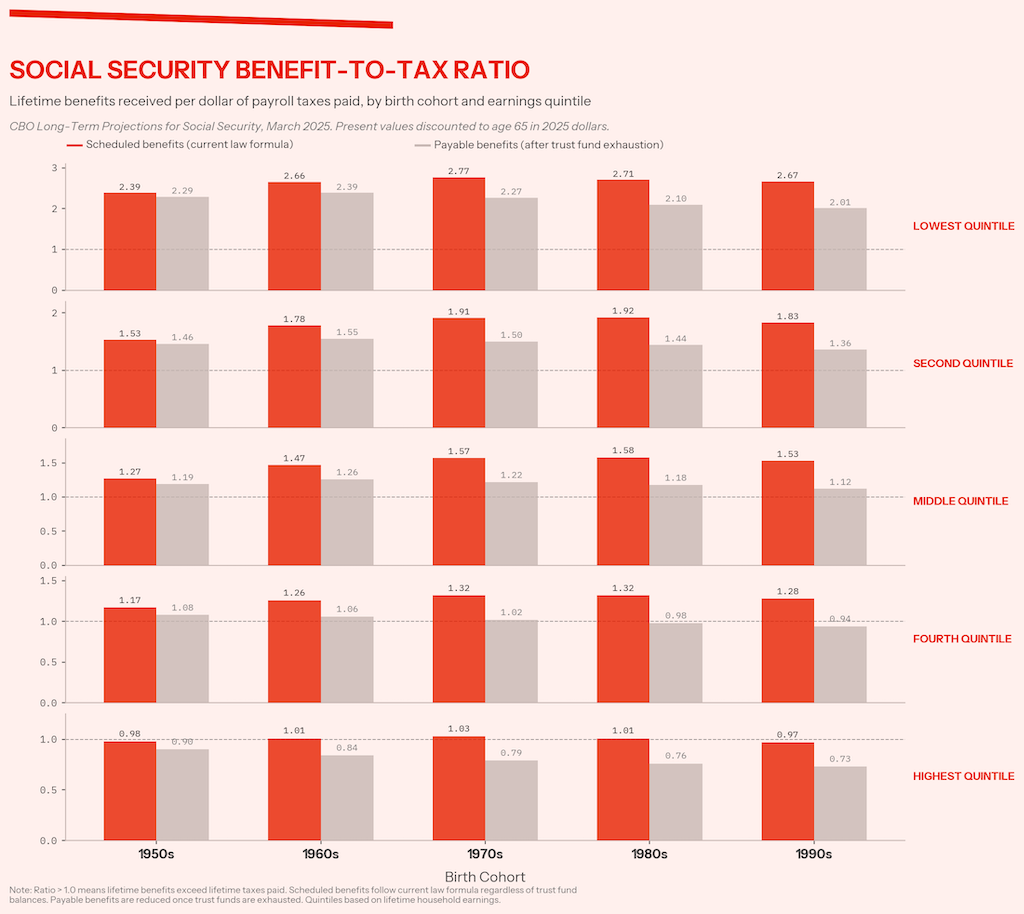

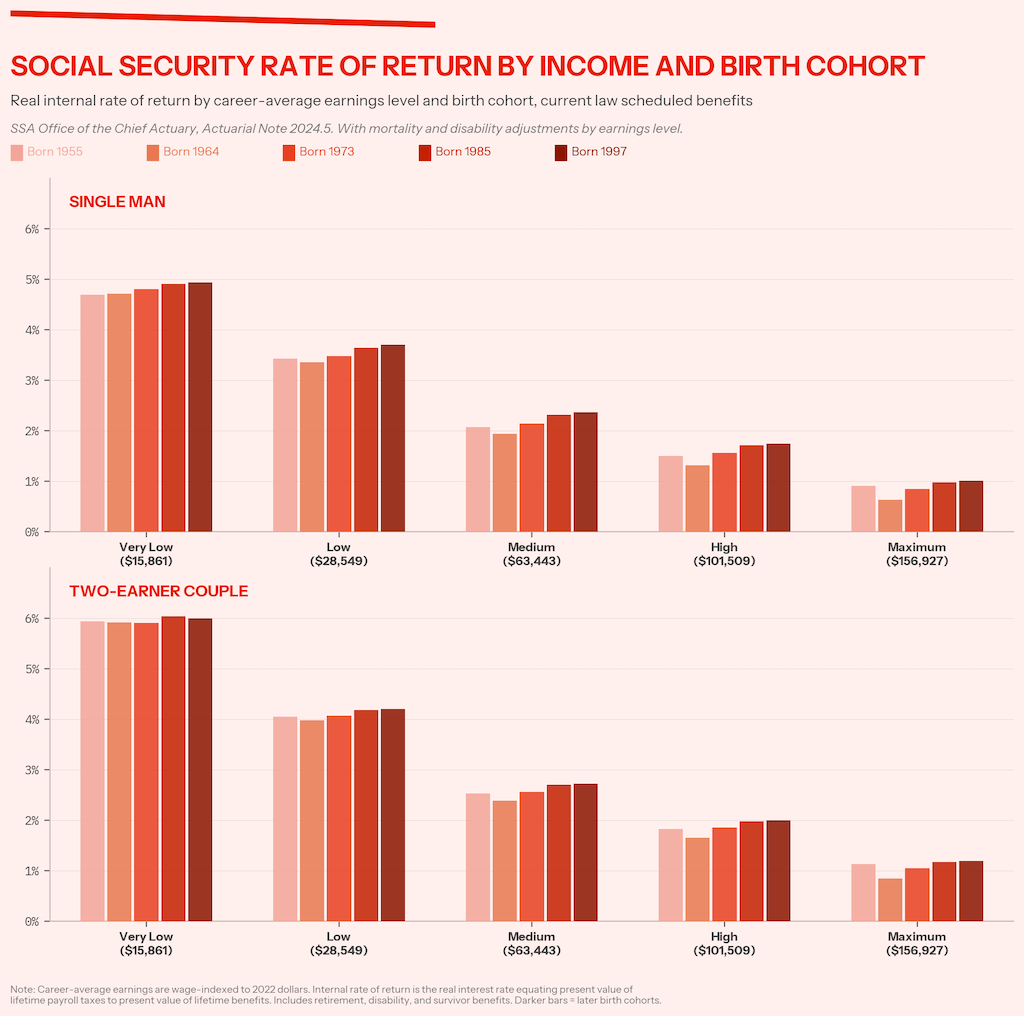

Contrary to the idea that Social Security is short-changing younger generations, the system is structured to be more generous to Americans born in the 1970s, 1980s, and 1990s — roughly Gen X and millennials — provided that benefits aren’t cut before they reach retirement age.

The nonpartisan Congressional Budget Office (CBO) publishes projections for Social Security that include lifetime benefits and lifetime taxes for each decade’s birth cohort and earnings quintiles. The projections include two scenarios: benefits scheduled under current law and benefits payable if Congress takes no action and lets across-the-board cuts take effect upon trust fund depletion.

The benefit-to-tax ratio shows whether each cohort and income group will receive more in lifetime benefits than it contributes in lifetime taxes, with both valued in 2025 dollars discounted to age sixty-five at the average interest rate on federal debt.

With the partial exception of the highest quintile, the three younger cohorts’ benefit-to-tax ratio exceeds the ratios for those born in the 1950s and 1960s, unless benefits are cut.

In other words, cuts to Social Security — not Social Security’s benefit structure itself — would make conservatives’ generational criticism of Social Security true. Other estimates of Social Security’s benefit-to-tax ratio by birth cohort reach the same conclusion.

The CBO’s benefit-to-tax ratio is also the source for claims like Ponnuru’s that workers receive “more than the sum of what the person paid in taxes and the interest on that money.”

Yet this raises an obvious question: If Social Security returns more than workers contribute, how can conservatives simultaneously claim that the program is a “very bad deal” and that, as President George W. Bush put it during his privatization push, workers’ “money will grow, over time, [in private accounts] at a greater rate than anything the current system can deliver”?

The CBO figures assume a real rate of return below 1 percent — specifically, the average interest rate on outstanding federal debt. This is the rate at which the federal government itself borrows money. It is not the rate that the Social Security trust fund earns on its reserves, which is roughly 2.6 percent.

It’s also not the effective rate of return that retirees of various income levels get on their payroll taxes. The Social Security Administration (SSA) does publish those internal real rates of return for workers of various income levels and birth years, though.

The SSA’s data shows that — even before considering market volatility and other downsides — it would be hard for private accounts to exceed Social Security’s returns for lower- and middle-income workers. That’s why studies that account for risk, fees, and transition costs find that privatization wouldn’t deliver better returns for most workers — particularly lower- and middle-income earners.

So the ultimate question is: How do we prevent the across-the-board cuts to Social Security that would, in fact, make it a worse deal for younger generations than older ones?

The answer reveals the central bait and switch of both the TBLC narrative and the entire “generational equity” framework. The only scenarios in which Social Security becomes a worse deal for younger generations are the ones TBLC proponents support, while the proposals that would ensure Gen Xers, millennials, and Zoomers are treated as well as — or better than — boomers are the ones they oppose.

Cutting Social Security (for Younger Generations)

Beyond outright privatization, conservatives’ preferred solution to Social Security’s seventy-five-year shortfall is to cut benefits. Specifically, conservatives have put forward numerous proposals to transform Social Security into a flat benefit, including Andrew Biggs’s $1,025 per month and Greene’s $1,250. Biggs, a staffer at the conservative American Enterprise Institute (AEI), has also endorsed proposals that would set monthly benefits at either 125 percent (about $1,660 per month for an individual and $2,250 for a couple) or 150 percent (about $2,000 per month for an individual and $2,700 for a couple) of the federal poverty level — the latter cited favorably by Ponnuru. Alternatively, Biggs has proposed retaining earnings-based benefits while imposing a roughly $3,500 per month cap.

With the exception of the $3,500 cap, all of these proposals would impose drastic benefit cuts on future retirees. Right now, nearly 90 percent of retired workers receive more than $1,025 per month, 80 percent more than $1,250, 75 percent more than $1,350, 60 percent more than $1,660, and half receive more than $2,000.

While flat benefits would boost benefits for those at the bottom, their value would erode over time. Currently, initial Social Security benefits are indexed to wage growth — something that conservatives have often criticized. Only the $1,025 per month proposal maintains that. The others that specify adjustments tie initial benefits to inflation. That means that flat benefit proposals level up fewer and fewer low-income retirees as each generation passes, since inflation tends to grow more slowly than wages. The $2,000 per month flat benefit would boost payments for approximately the bottom 40 percent of the 1970s cohort but only the bottom 20 percent of the 1990s cohort.

In fact, the vast majority of workers in the post-1960s cohorts would actually be better off with the automatic across-the-board cuts than with the lower flat benefit proposals. Even with the most generous flat benefit of $2,000 per month, 60 percent of the 1990s cohort would be better off with the across-the-board cut.

Previous Republican plans don’t fare better in terms of progressivity or “generational equity.” Paul Ryan’s aforementioned “Roadmap for America’s Future” proposed a variety of changes to Social Security. Ryan’s plan would’ve partially indexed initial benefits to inflation rather than wage growth, raised the retirement age for younger workers, and indexed yearly benefit growth to a version of the Consumer Price Index (CPI) that grows more slowly — despite the fact, as noted above, that elderly people tend to face higher rates of inflation. This would all come on top of partially privatizing the program.

The combined effects of the three benefit changes would’ve cut benefits by age seventy-five for retirees born in 1985 by 11 percent for a low earner (approximately $19,000 in 2010 dollars), 26 percent for a medium earner ($43,000), and 33 percent for a high earner (high earner ($69,000). Ryan’s cuts would be deeper for younger cohorts, growing by roughly 4 to 8 percentage points per decade depending on earnings level.

Nor did the private accounts rescue the plan. The CBO modeled the private accounts against the payable, rather than scheduled benefits, baseline; that is, it assumed that benefit cuts would take place upon the trust fund’s depletion. Even then, it projected that most younger generations would be no better off under Ryan’s plan than under the automatic cuts themselves — and worse off compared to what they’d been promised under scheduled benefits.

The Simpson-Bowles proposals changed Social Security’s benefit formula, raised the retirement age, introduced a new minimum benefit, and switched to the same slower-growing CPI used in Ryan’s plan, along with slightly increasing the payroll tax cap.

The commission’s plan went through several revisions, but the final version analyzed by the SSA would have raised benefits at age seventy-five for approximately 30 percent of low-income retirees born in 1985, while cutting benefits for everyone else. A medium earner would’ve seen a cut of 15 percent, a high earner 30 percent.

The cuts deepened both with income and each succeeding generation. Benefits for all workers would converge to a narrow range between $850 and $1,250 per month. As the Center on Budget and Policy Priorities put it, “In the long run, most workers would end up getting very similar benefits, despite having paid very different amounts in payroll taxes.”

In 2016, Republican Sam Johnson, the chair of the House Ways and Means Subcommittee on Social Security, put out a proposal with many of the same changes as Simpson-Bowles, except that it eliminated cost-of-living adjustments for higher-income retirees and eschewed any tax increases. For those born in 1985, a new minimum benefit would have slightly boosted benefits for roughly 25 percent of low-wage workers but imposed cuts on most — between 17 and 28 percent for a medium earner (approximately $50,000 in 2016 dollars) and 33 percent for a high earner ($80,000). It also proposed raising the full retirement age to sixty-nine by 2030.

Raising the retirement age is, in fact, central to virtually every conservative or centrist Social Security proposal, even though increases in longevity have been concentrated among upper-income Americans. As one study summarized, today “the richest American men live fifteen years longer than the poorest men, while the richest American women live ten years longer than the poorest women.”

In other words, raising the retirement age would concentrate its costs on poor and working-class members of younger generations — the very group that proponents of “generational equity” claim to care about most. It is, in effect, a benefit cut engineered to fall hardest on the millennials stocking shelves and driving trucks, and lightest on those managing hedge funds.

All the same, these proposals were touted by conservative think tanks and Peterson-backed groups focused on deficit reduction and generational accounting. The CRFB, for example, praised Ryan’s “Roadmap,” arguing that he “deserves a blue ribbon for fiscal courage.” The CRFB’s senior policy director, Marc Goldwein, served on the Simpson-Bowles commission’s staff, and the CRFB wrote that Johnson “should be commended for putting forward a serious plan to make Social Security financially sustainable.”

The CRFB’s own 2019 Social Security proposal — drafted by MacGuineas, Goldwein, and Chris Towner — incorporated elements of the Ryan, Simpson-Bowles, and Johnson plans, including an altered benefit formula, a slower-growing measure of inflation, an increased retirement age, and add-on private accounts. The proposal is billed as “maximiz[ing] generational fairness.”

For all their talk of “generational equity,” the originators of TBLC-style narratives have consistently championed plans that impose nearly all of their cuts on younger generations. Few of the proposals they praise would apply changes to current retirees, the demonized boomers.

MacGuineas made this explicit in her recent Senate testimony, assuring Americans that “current seniors do not need to worry about [cuts].” Even cuts that do apply to current retirees, such as the Simpson-Bowles CPI change, would hit younger generations harder, since the boomers have already collected a substantial share of their benefits. Tellingly, the CRFB praised Johnson’s proposal even though it would’ve boosted the incomes of rich boomers by eliminating income taxes on Social Security benefits — a provision that currently only affects upper-income retirees.

What gives?

The truth is that most of Social Security’s critics would prefer that the program didn’t exist. That their reform proposals result in a system that’s a terrible deal for younger generations is a feature, not a bug. The worse Social Security becomes, the more likely it is that future generations will eventually turn against it and embrace privatization.

They’re also anxious to avoid tax increases — at least on the rich. As Greene noted, proponents of the TBLC framework want to “align Wall Street, the defense industrial complex, corporate America, and the media against TBLC,” because “the alternative is tax hikes.”

In a November essay, “Start Demagoguing Against the Old,” which has been cited by Greene, erstwhile far-right provocateur Richard Hanania put the stakes in stark terms. He argued that the popularity of Social Security and Medicare proved that “you should have contempt for the political views of most people.”

According to Hanania, “there’s nobody less deserving of being the beneficiaries of the welfare state than the old,” because “poverty becomes more blameworthy with age.” Hanania warned that unless the public could be persuaded that “the energies of the young and productive are [being] sucked dry to continually make life more and more comfortable for those on death’s door,” the result would be “anti-rich demagoguery” and tax hikes on the well-off.

Indeed, both the CRFB and Third Way have framed raising taxes on the rich as a mythical solution to Social Security’s shortfall, and AEI’s Biggs has written, “If there were an easy way to fix Social Security, it would have been done by now.”

But raising taxes on the rich is the “easy way.” It’s just that these organizations — and, especially, their wealthy donors — don’t want it to happen.

Saving Social Security by Taxing the Rich

The overarching public policy goal of the American political right and the Republican Party for the past five decades has been cutting taxes for the rich. From Reagan’s 1981 tax cuts through Bush’s 2001 cuts to Trump’s 2017 and 2025 cuts, the first thing almost every Republican president does upon taking office is pass a top-heavy tax cut.

As a result, each time Republicans have left the White House, taxes on the rich have been lower than when they entered. Amid shifting positions on issues like trade and immigration, it’s the one thing that Republicans can agree on.

Besides soaring incomes for the rich, the upshot has been worsening deficits over the course of each Republican president’s team since Reagan. Far from accidental, this has been part of a concerted conservative strategy to “intentionally increase the national debt through tax cuts in order to bind the hands of a subsequent liberal government,” as Bruce Bartlett has summarized. This strategy has largely succeeded in turning Democratic presidents into deficit-conscious “Eisenhower Republicans” by the end of their terms, with the encouragement of the aforementioned corporate-backed “deficit hawk” groups.

But in recent years, Republicans’ strategy of passing bills that pair a huge tax cut for the very rich with small ones for lower- and middle-income Americans has hit a snag. After decades of cuts, federal income taxes — as opposed to regressive payroll, state, and local taxes — are too low on most Americans for there to be much to cut. In response, Republicans at the national level have borrowed a strategy from their counterparts at the state level: pairing tax cuts for the rich with tax hikes on the poor.

Just as Ryan’s “Roadmap” would have dramatically boosted incomes at the top while cutting them for the middle class, both 2017’s Tax Cuts and Jobs Act (TCJA) and 2025’s combination of the One Big Beautiful Bill Act (OBBBA) and tariff increases have followed the same pattern: lowering federal taxes for the rich while raising them on nearly everyone else.

The TCJA even borrowed a tool from conservative Social Security proposals, switching the inflation measure used to index tax brackets to a slower-growing one, producing “bracket creep” that will gradually push lower- and middle-income taxpayers into higher brackets over time, a stealth tax increase that even the Cato Institute has criticized in the past. The OBBBA and tariffs are starker still. According to the Budget Lab at Yale, the combined effect is a reduction in income for the bottom 90 percent of households and an increase for the top 10 percent.

Republican Senator Ted Cruz is even pushing Trump’s Treasury to unilaterally cut capital gains taxes by allowing taxpayers to subtract inflation from their gains. This proposal has been rejected by several Republican administrations in the past as an unconstitutional usurpation of Congress’s power of the purse, but there’s no telling what might happen today. Slashing capital gains taxes has been one of the Right’s primary goals since the 1970s, and the benefits of Cruz’s proposal would accrue almost wholly to the top 1 percent.

Democrats must break the cycle of top-heavy tax cuts, and the Social Security payroll tax cap is the perfect place to start.

Social Security’s projected seventy-five-year shortfall is roughly 1.3 to 1.5 percent of GDP. To put that into perspective, the United States spends 7.3 percent of its GDP on old-age pensions and survivors’ benefits. Contrary to TBLC proponents’ claim that Social Security is too generous, that’s below the thirty-eight-country OECD average, as is the share of recipients’ pre-retirement income replaced by Social Security.

Where is the US below average? Revenue. The average country of the Organisation for Economic Co-operation and Development (OECD) collects 34.1 percent of its GDP in taxes, while the United States collects just 25.6 percent, and the gap between the United States and the OECD average has grown in the past twenty-five years.

The SSA publishes a comprehensive list of proposed changes to Social Security, and the CRFB incorporates some of them into its interactive Social Security “Reformer” tool. Looking at either, the inescapable conclusion is that the single easiest way to improve Social Security’s long-term solvency is to eliminate the payroll tax cap without proportionally boosting benefits for the rich. This single change would eliminate two-thirds of Social Security seventy-five-year shortfall. Amusingly, President Bush floated the idea of raising the cap, provided the revenue went toward his private accounts.

Why does removing Social Security’s payroll tax cap have such a large effect? Because income inequality has soared in the past fifty years. As a larger and larger share of total income flows to the rich, more of it escapes Social Security taxation. In 1983, 10 percent of income was above the cap. Today, more than 16 percent is. Compared to other OECD countries, our payroll tax cap is low.

While eliminating the Social Security payroll tax cap isn’t a popular change with conservatives, it is with the public. Many Americans don’t even know that Social Security’s payroll tax is capped. Currently, Americans don’t pay Social Security payroll taxes on income above $184,500. Only about 6 percent of workers a year make more than that. In other words, a tax increase that only affects the richest 6 percent of Americans each year would fix 67 percent of Social Security’s seventy-five-year shortfall.

This is also the most popular reform according to polls. Throughout the Bush- and Obama-era reform debates, between two-thirds and 80 percent of Americans supported eliminating the cap. Recent surveys have found similar proportions.

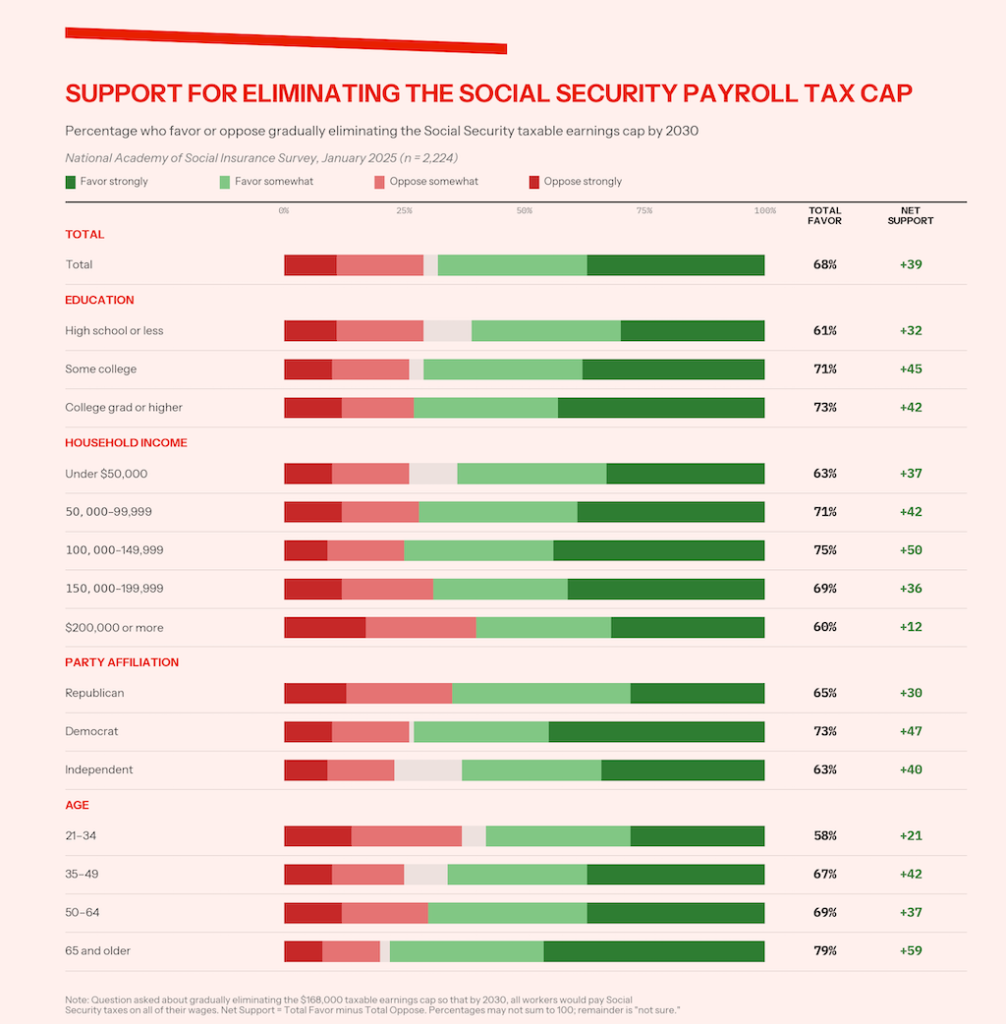

The most notable is a recent National Academy of Social Insurance (NASI) survey that used trade-off analysis “to learn which of various packages of Social Security policy changes Americans want and are willing to pay for, via their impact on the financing gap.” Unlike single-issue polling, this “forces respondents to weigh the costs of options holistically versus considering individual options in isolation.”

The NASI found that eliminating the Social Security payroll tax cap was the most popular reform idea, favored by 68 percent of respondents, including majorities of all income, age, education, and political groups. As NASI summarized, “By far respondents’ greatest aversion is to any reform package that does not change the payroll tax cap.”

The NASI tested both a total elimination of the cap and lifting the cap above $400,000. The latter proposal would leave an untaxed “donut hole” between $184,500 and $400,000 but would comply with President Joe Biden’s foolish pledge not to raise taxes on the middle class, which he preposterously implied extended to $400,000. The NASI’s study, though, found that a total elimination was more popular than the $400,000 threshold.

Even a recent Cato Institute survey question that primed a negative reaction by saying that eliminating the Social Security payroll tax cap “would cover only part of the shortfall and could discourage work” found 2:1 support for its elimination, which is perhaps why Cato left the question out of its report.

The public’s views on eliminating the Social Security payroll tax cap are part of a broader pattern of public support for raising taxes on the rich and opposition to cutting Social Security or Medicare. According to the NASI study, “Respondents also have a strong aversion to any reform package that increases the retirement age to 69 or reduces the cost-of-living adjustment — two policies that would reduce benefits.” Indeed, 64 percent said they wanted Social Security to adjust benefits according to the faster-rising inflation measure that better reflects seniors’ cost of living.

Most Americans would even prefer raising their own payroll taxes to cutting Social Security. The NASI study, for example, found that “only 15 percent of respondents say we shouldn’t raise taxes on any American even if it means reducing benefits.” Fifty-seven percent specifically supported gradually raising the payroll tax rates by 2 percentage points.

This change would eliminate 39 percent of Social Security’s seventy-five-year shortfall. It would also be better for Americans born in the 1970s, 1980s, and 1990s than automatic cuts or any of conservatives’ flat benefit proposals. An immediate increase of 1.25 points would eliminate roughly a third of the shortfall, while also ensuring that the vast majority of those cohorts would also enjoy higher benefit-to-tax ratios than those born in the 1950s.

The Cato survey ironically ended up reaching similar conclusions, despite seemingly intending to generate a Luntz-like UFO viral talking point. The few news stories on Cato’s survey writeup foregrounded a “generational divide” on Social Security based on a question framed to suggest that younger generations preferred cutting benefits to raising taxes. However, Cato’s report noted that “Americans under age 30 are about as likely as older Americans to support increasing taxes to maintain Social Security benefits.” Only when another question posited a scenario where they “would eventually get back less than they paid in” did younger respondents turn against tax hikes.

Moreover, even if younger Americans were to express a relative willingness to cut Social Security, that doesn’t mean it’s a durable viewpoint. Decades of propaganda have told them the program won’t be there for them, and younger people tend not to worry much about a retirement that’s still decades away. During Bush’s Social Security privatization push, some polls found that most Gen Xers were open to private accounts. But those are now the same fiftysomethings strongly opposed to cuts, according to both the NASI and Cato surveys.

Even if Americans of all ages are willing to raise their own payroll taxes, that option should take a back seat to taxing the well-off, which is essential to addressing the real inequality in the United States — the gap between rich and poor, not young and old.

Distributional Fairness Trumps “Generational Fairness”

Both marginal and effective tax rates on the ultrarich have fallen sharply since the “Great Compression” of the mid-twentieth century, when income inequality in the United States was low and average workers enjoyed strong real wage growth. Today the richest Americans often pay lower effective tax rates than the middle class, whether measured against their income or their wealth.

Soaring inequality has reshaped the income distribution. Since 1979, real incomes of the middle class have grown 65 percent after taxes and transfers, while those of the very richest have grown by more than 600 percent, according to the CBO. This may even understate the gap, considering that the well-off tend to face lower inflation rates than those further down the income distribution.

One recent study found that while the income gap between the richest and poorest households grew 16 percent between 2002 and 2019 according to typical cost-of-living measures, it rose to 23 percent when accounting for the unequal inflation rates faced by different households.

Conservatives have dubiously attempted to downplay these trends. They also insist that raising taxes on the rich will harm economic growth, even if it reduces inequality. But there’s little reason to take these arguments seriously.

Falling taxes on the rich have fueled rising inequality not only by directly boosting their after-tax incomes but also by indirectly incentivizing their rent-seeking behavior — extracting wealth rather than creating it. Research shows that “a lower top tax rate increases the rate of return to efforts demanding greater compensation from boards of directors,” as economist Andrew Fieldhouse has summarized.

These boards are often composed of fellow executives, creating a mutual back-scratching dynamic that professor Edward Lawler has captured well. “You don’t have to be a compensation expert to realize that if you vote for one of your peers to have a higher salary, you are in effect voting for your own salary to go up, because it is based on what will be a higher market,” he notes. CEO pay has skyrocketed 1,322 percent since 1978, pushing the CEO-to-worker compensation ratio from 31:1 in 1978 to 281:1 today.

Making matters worse, numerous studies have found that the ultrarich then use their inflated incomes to lobby for tax cuts and other policies that further enrich them. Since the Supreme Court gutted campaign finance laws in the 2010 Citizens United v. FEC decision, the influence of the rich in US politics has exploded. Prior to Citizens United, the share of spending on federal elections by three hundred billionaires and their families was just 0.3 percent. By 2024, it had jumped to 14 percent.

This has exacerbated politicians’ preexisting tendency to cater to the preferences of the rich. As one team of researchers found that “politicians who receive a larger share of their campaign funding from the top one percent donors are more likely to shift their voting toward the preferences of the wealthy,” especially on economic issues “such as taxation, regulation, and social welfare programs,” where “top earners have more convergent — and mostly conservative — views.”

The result is a vicious cycle whereby each inequality-driven increase in political donations leads to the enactment of policies that boost the incomes of the well-off, which begets a further increase in their donations and another round of inequality-increasing policies.

As political scientists Adam Bonica and Howard Rosenthal have explained, “If Republicans promote policies — such as tax changes — that make their current donors immediately wealthier, they can expect a proportional increase in total donations.” Ultimately, as another study concluded, “The erosion of tax progressivity has contributed to raise the political clout of wealthy individuals, via campaign donations,” creating a “spiral between economic inequality and uneven political influence.”

Nor is it clear that raising taxes at the top will harm economic growth, despite the claims of conservative “supply–side“ logic. The most persuasive evidence finds no support for the idea that low taxes on the rich increased economic growth.

A recent widely cited study by David Hope and Julian Limberg of the London School of Economics looked at the economic effects of major tax cuts for the rich in eighteen wealthy countries over a fifty-year period. They found that cuts reliably boosted the incomes of the rich but influenced GDP and employment at a level that was “statistically indistinguishable from zero.” Indeed, a growing body of research suggests that, contrary to conservatives’ claims, income redistribution and lower inequality actually improve growth.

Even if raising taxes on the rich were to pose a trade-off between growth and equality, it’s not clear why most Americans should prioritize the former over the latter. Over the past five decades, the benefits of rising GDP and productivity have flowed to the top. In a 2017 study of the distribution of economic growth in the United States since World War II, economist Pavlina Tcherneva found that “with every postwar expansion, as the economy grew, the bottom 90 percent of households received a smaller and smaller share of that growth.”

The tight labor market and redistributive policies of the COVID-19 pandemic temporarily reversed this trend, but the gains for lower- and middle-income workers have already begun to erode — a trend that President Trump’s regressive tariffs and top-heavy tax cuts have exacerbated.

That trend is directly related to the incentives created by low taxes on the very rich. As Fieldhouse explained, executives’ “successful efforts [to boost their compensation] will come out of workers’ paychecks, not shareholders’ portfolios.” By one estimate, rising inequality since 1979 has cost middle-income households roughly $40,000 per year.

This inequality, rather than too-slow growth, is also the primary cause of younger generations’ declining odds of earning more than their parents in real terms. As the New York Times explained, the research team studying intergenerational mobility

ran a clever simulation recreating the last several decades with the same GDP growth but without the post-1970 rise in inequality. When they did, the share of 1980 babies who grew up to out-earn their parents jumped to 80 percent, from 50 percent. The rise was considerably smaller (to 62 percent) in the simulation that kept inequality constant but imagined that growth returned to its old, faster path [of the early post-WWII decades].

Beyond their economic and political effects, taxes on the rich need to be raised to restore faith in the tax system. For decades, large majorities of the public have told pollsters that large corporations and rich individuals don’t pay their fair share of taxes. With leak after leak exposing the elaborate tax avoidance schemes of the ultrarich and President Trump declaring that escaping federal income taxes “makes me smart,” it’s easy to see why the public is cynical about the fairness of the tax system.

From President Clinton’s “Reinventing Government” initiative to Trump’s Department of Government Efficiency (DOGE) fiasco, both Democratic and Republican presidents have been obsessed with rooting out supposed waste, fraud, and abuse in the federal budget to restore faith in government spending. But what about faith in the tax system? A recent Internal Revenue Service (IRS) survey found that more than 70 percent of Americans said that focusing on wealthy individuals and corporations who exploit tax loopholes would help ensure that other taxpayers “pay their taxes honestly.”

A cynical public might be willing to pay higher taxes for overwhelmingly popular programs like Social Security but not for other worthy policies. Republicans understand this. When President Biden attempted to reduce tax avoidance by the rich by increasing IRS funding, conservative groups organized against it, despite its popularity. Republicans then worked to rescind it piece by piece at the same time that they were inserting new loopholes to benefit the rich.

Congress hasn’t attempted major loophole-closing tax reform since 1986, and even that reform largely undid its loophole-closing effects by dramatically cutting rates on upper-income earners. But unless Democrats restore faith in the tax system, they’ll remain trapped in the anti-tax logic and donor-legislation feedback loop that reliably benefits the Right.

Beyond eliminating the Social Security payroll tax cap, Democrats have plenty of options to address the program’s remaining shortfall and fund other priorities by raising taxes on the well-off.

Viewed yearly, Social Security’s shortfall currently totals approximately $450 billion, with annual deficits closer to $250 billion today and larger ones in later years. The yearly “tax gap” — taxes owed that go uncollected — is somewhere between $650 billion and $1 trillion per year. This gap is driven primarily by tax avoidance among the wealthy, and tougher IRS enforcement could close a substantial portion of it.

Democrats should also focus on eliminating “tax expenditures” that benefit the well-off. The exclusion for employer-sponsored retirement plans and IRAs costs between 0.9 and 1.3 percent of GDP each year. Research shows these tax incentives do little to boost retirement savings, and the benefits flow disproportionately to the well-off. As the CBO has reported, “Households in the highest quintile received more than 60 percent of the benefits of the income tax expenditure. The two lowest quintiles together received less than 5 percent of the benefits.”

A bipartisan trio of scholars has proposed wholly or partially eliminating this tax expenditure and redirecting the savings to shore up Social Security. They note that “rollbacks of the ineffective retirement saving tax preference could fill a substantial portion of Social Security’s long-term funding gap.”

The preferential rate on capital gains is nearly as large as the retirement tax expenditure and tilted even more toward the top, flowing almost wholly to the richest 1 percent. Given how skewed capital gains are, many Americans are likely unaware that investment income is taxed at a lower rate than labor income, and surveys show that most Americans support eliminating the preference.

Effectively eliminating the capital gains preference is challenging, given that the rich can change their realization patterns to avoid higher rates. However, a wealth tax, financial transactions tax, or mark-to-market taxation of investment income are viable responses. In terms of Social Security, the SSA has modeled five different options for taxing investment income to fund Social Security, using rates of either 6.2 or 12.4 percent. Depending on the specifics, these changes could close between 18 and 48 percent of Social Security’s long-term shortfall.

To create real intergenerational equity, Democrats should also fix the estate tax. Currently, only the wealthiest 0.14 percent of estates owe any tax, a share that’s fallen in the past twenty-five years due to a series of Republican-led cuts. But the estate tax is the most progressive tax in the US tax system.

Given TBLC proponents’ professed concern about the unfairness of boomers’ wealth, they should support using the estate tax to capture the upcoming “great wealth transfer” set to occur when boomers pass away. Failure to adequately tax inherited wealth “increases wealth inequality within generations and amplifies the inequality due to intergenerational wealth transfers.” If the United States reverted to its 2001-era tax laws, the inheritance tax would have raised $145 billion, rather than $18 billion, in 2021.

In addition to higher rates, the current system could be improved by converting the estate tax to an inheritance tax, which would “raise revenue, increase progressivity, broaden the income tax base, improve equity, and boost economic mobility,” as a recent Brookings Institution study summarized.

A key piece of effective reform is eliminating the “stepped-up basis” loophole, which allows the wealthy to pass investments to their heirs without ever paying capital gains taxes on the gains accrued during their lifetime. The best way to eliminate that loophole would be to tax unrealized gains at death, which would raise roughly $536 billion per decade, according to the CBO.

Democrats should also undo many of the recent cuts introduced by Trump and congressional Republicans. Beyond reversing cuts to top brackets, Democrats should repeal the corporate tax cut known as 100 percent bonus depreciation, which is expected to cost $362 billion per decade, as well as the hollowing out of Biden’s corporate minimum tax, which was projected to raise $222 billion per decade.

Particularly if the payroll tax cap is removed, only a fraction of the above reforms would be needed to fix Social Security’s long-term shortfall. But policymakers should consider directing some of the revenue raised from progressive tax reform toward rebuilding Social Security’s “Missing Trust Fund.”

The great irony of demonizing boomers as the source of Social Security’s shortfall is that scholars have long known that the real beneficiaries of intergenerational inequity in the program were the Lost Generation and Greatest Generation. Americans who retired in Social Security’s first few decades received far more in benefits than they had contributed, a windfall that consumed not only the reserves that would have accumulated but also decades of compound interest on those reserves. The Silent Generation, boomers, and every cohort that followed have been paying for that gift.

The 1939 restructuring of Social Security that benefitted those early generations shifted the program from a funded system toward pay-as-you-go financing. The cost of those missing reserves has been baked into payroll tax rates ever since.

According to research by Alicia Munnell and colleagues at the Boston College Center for Retirement Research, this “Missing Trust Fund” now stands at roughly $27 trillion. Its absence is why Social Security’s payroll tax rate is approximately 3.7 percentage points higher than it would otherwise need to be. Had Congress eliminated the payroll tax cap in 1939, payroll tax rates might be lower today, and we might not be talking about a shortfall at all.

One ambitious solution would be to rebuild the “Missing Trust Fund” and invest it in assets with higher returns than the low-yield Treasury securities the trust fund currently holds, thereby creating what amounts to a sovereign wealth fund (SWF) for Social Security.

Munnell suggests that a 2.3 percent income tax increase would be the fairest mechanism for funding it. There are other options for creating a SWF. Democratic Senator Tim Kaine and Republican Senator Bill Cassidy have recently proposed allowing the government to borrow and invest in stocks and bonds — a less-than-ideal version of the same concept, since it relies on borrowed rather than dedicated revenue.

Whether any of these plans would be worth the risk would depend on the fund’s political independence, among other factors. But it’s hard to imagine today’s Republicans supporting an idea they deemed too socialistic when it was proposed by President Clinton, or progressive Democrats risking Social Security’s guaranteed character without an ironclad guarantee that the Treasury would backfill any investment losses with general revenue.