German Deindustrialization Is Self-Inflicted

Germany is in the midst of an industrial job loss wave worse than the one during COVID. The Right blames the green transition, and parts of the Left blame the Ukraine war. But the real cause is the shortsightedness of Germany’s political elite.

Friedrich Merz and powerful political factions in Germany still believe that averting the country’s decline requires a race to the bottom on wages and regulations. (Christian Ender / Getty Images)

The specter of deindustrialization has been haunting German political discourse since the late 2010s. Across the political spectrum, the supposedly imminent demise of German industry has largely been attributed to the country’s numerous energy policy failures. Depending on whom you ask, the principal cause is the absence of “cheap” Russian pipeline gas, a general dependence on fossil fuels, or, conversely, the expansion of renewable energies. These arguments have gone unexamined for years — until now.

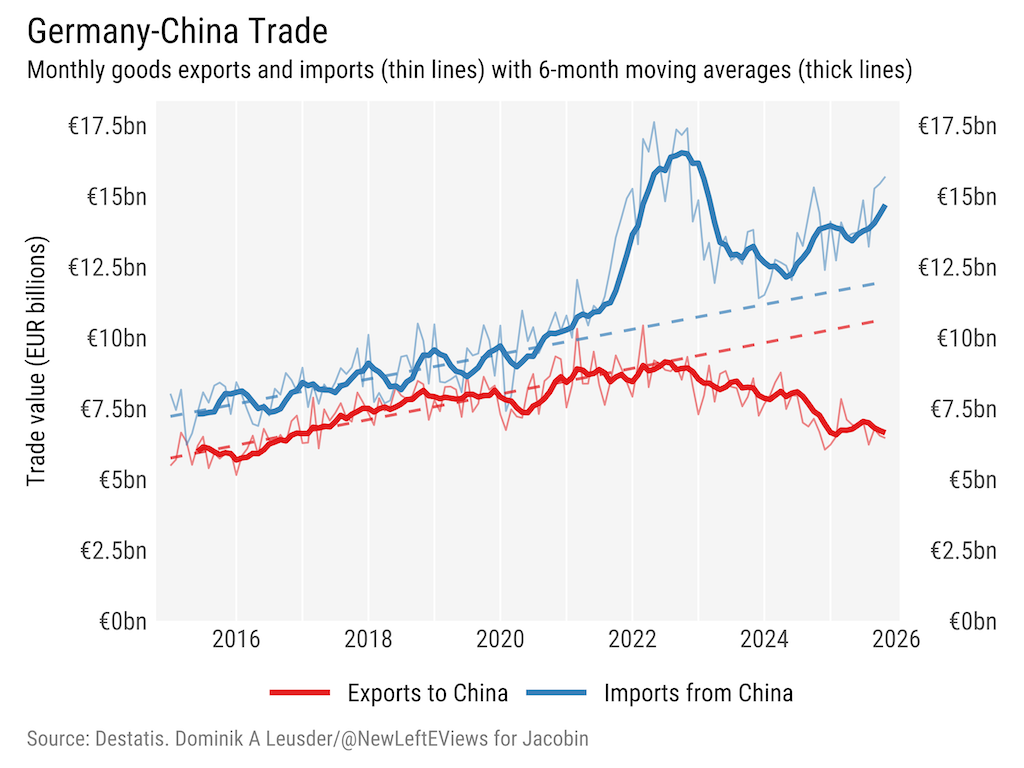

It is starting to become clear that the main reasons lie elsewhere. In an ironic twist, the repeat offender when it comes to running persistent export surpluses has been falling prey to its growing trade imbalances with China: goods imports are displacing German production while exports to China have been falling. The recent dramatic worsening of this imbalance is driven by an intensification of Chinese industrial policy. But years of self-destructive underinvestment and austerity in Germany have greatly exacerbated the situation.

It is not clear that German chancellor Friedrich Merz, who was in Beijing last week to discuss the two nations’ trade relations, has the right diagnosis of his country’s malaise. Though he is now alive to the importance of bilateral trade with China, Merz and powerful political factions in Germany and Europe still believe that averting Germany’s decline requires a race to the bottom on wages and regulations. This begs a number of questions: What has actually been driving deindustrialization; what role has China played; how should Sino-German relations be transformed; and should Germany emulate China, as China once did Germany?

Signs of a Deeper Crisis

The decline of the German industrial sector is mainly a phenomenon of the 2020s. Previously, there were pessimistic rumblings. In 2017, prominent conservative economist Hans-Werner Sinn had prophesized that the energy transition would turn Germany into an “industrial park.” But despite a general weakness in industrial production in 2018 and 2019 (which was more due to one-off factors), there was nothing to indicate a deep crisis.

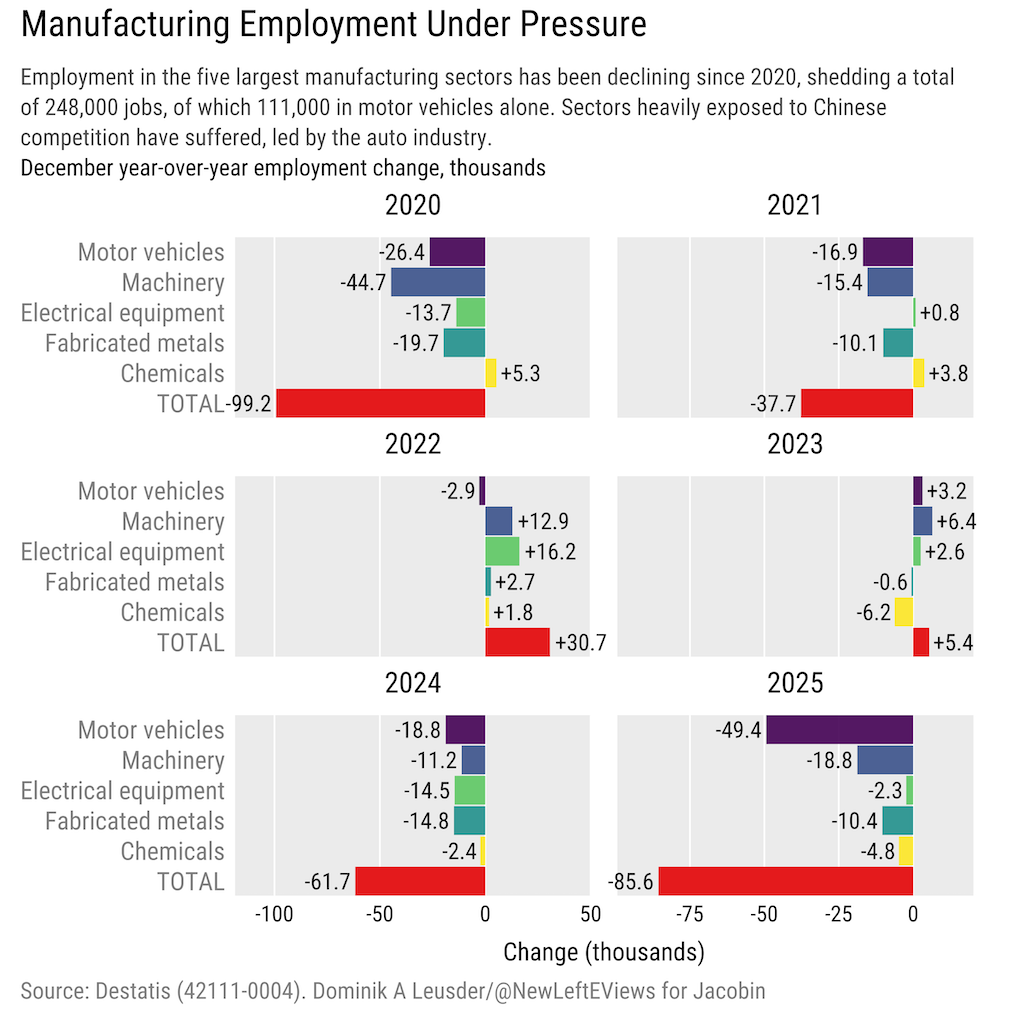

But the years since 2020 paint a different picture: industrial employment has cratered. Up to and including December 2025, 248,000 jobs have been lost in Germany’s key industrial sectors: motor vehicles, machinery, electrical equipment, electronics, fabricated metals, and chemicals. They have been regarded as the crown jewels of European industry and have inspired emulation in developing countries. The biggest losses were in the automotive sector, where 111,000 workers were laid off, accounting for about 13.4 percent of the sector and 42 percent of total manufacturing job losses since November 2019.

Alarmingly, these figures conceal the extent of the decline in employment. As the most export- and energy-intensive sector, the chemical industry is emblematic of the two biggest weaknesses of the German economy. Plagued by strong international cost competition and the rise in gas prices since the Russian invasion of Ukraine, the chemical industry (which uses gas not just for energy but for its feedstock) has recorded a continuous decline in production, exports, and orders since 2019. In addition, capacity utilization has fallen to 70 percent as of 2025, as production lines for base chemicals such as ammonia and polymers are shut down until further notice.

At the same time, however, employment has remained relatively stable. That’s partly because the decline in one segment has been masked by job growth in the pharmaceutical sector, suggesting adaptability. The main reason, however, seems to be the groaning German labor market. Due to the ongoing shortage of skilled workers, companies are hoarding qualified employees and weighing the costs of higher current payrolls against the uncertainty and costs of training new employees in the future.

The Service Sector Is Not a Panacea

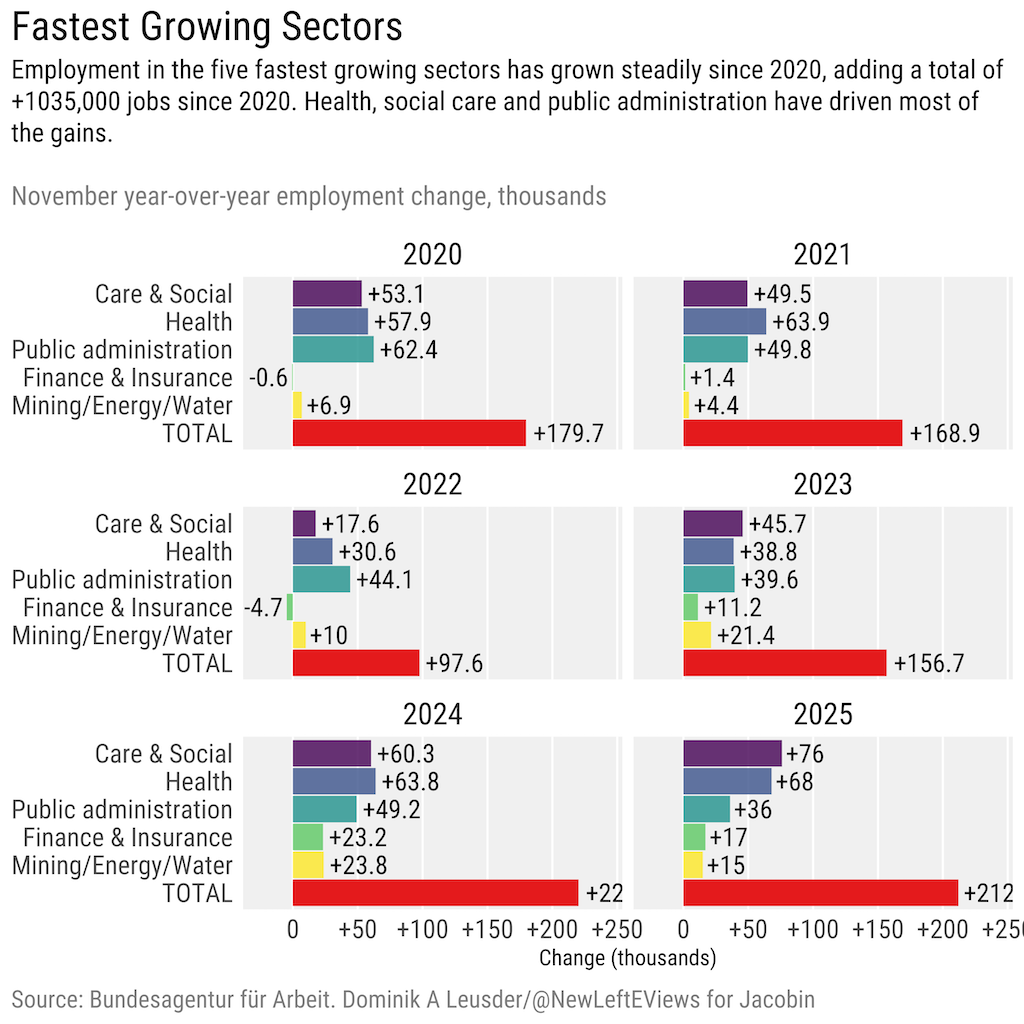

The official unemployment rate reached 6.6 percent in January. A closer look, however, shows that the composition of employment in Germany is changing. Since 2025, more than one million new jobs have been created, mainly in the care and social services, health care, and public administration sectors. Economic historian Adam Tooze argues that the slow but steady shift toward services could be a sign that the German economy is “normalizing.” He recalls the discourse of the “blocked society” (Blockierte Gesellschaft) in the 1990s, a phase of high structural unemployment and high social spending, which Germany eventually overcame, shedding the image of the “sick man of Europe.” Meanwhile, the Economist magazine argues, more fervently but less convincingly, that Germany should adopt Britain’s service-based growth model wholesale.

Britain is the prime example of a country that, despite a large service sector with highly productive services (such as IT, consulting, and finance), is trapped in a vicious cycle of low investment, productivity, and real wage growth as well as high inequality. This reflects that the so-called “productive” services are accompanied by high exploitative rents (from capital income) that inhibit economic activity in other areas while driving up asset prices.

The UK economy is paradigmatic of the “dual” or permanently “K-shaped” type of economy, in which income gains benefit the top 20 to 30 percent (but especially the top 10 percent) while the rest stagnate or shrink in the face of rising living costs. While Germany has not been exempt from these trends (inequality has been increasing and wealth disparities are anomalously high), a UK-ification of its economy would worsen them.

The relative indifference to deindustrialization from the liberal center can hardly be justified. A long-term decline in productivity and real wage growth, especially in a rapidly aging society, would not only further weaken the middle class and drive up poverty, but it would also call into question the long-term sustainability of what remains of Germany’s social welfare. The statements by some commentators that Germany — and, in the larger scheme, Europe — simply has to “accept decline” and “culturally adapt” to economic stagnation is at best unserious and at worst nonsensical. But can uncontrolled industrial decline be stopped at all?

Energy Prices Are Not the Main Problem

The most widespread explanation for Germany’s industrial malaise has focused on electricity prices. Put simply, more costly energy inputs render production more expensive, which either blunts export demand for more costly final goods or cuts into profits. In view of falling profits, new investments in the expansion of productive capacity cannot be guaranteed. Indeed, in addition to employment, capacity utilization and market shares of German companies are falling.

This criticism usually refers both to the energy transition, with regard to the impact of renewable energies on the overall energy mix, and to energy and foreign policy in relation with Russia and the United States. Alice Weidel, leader of the surging far-right Alternative für Deutschland (AfD), holds to both narratives: climate policy as “nothing more than a monstrous deindustrialization program” and the sanctions program against Russia as an “economic war against Germany.”

On the party-political left, the industrial decline is widely seen as the result of Germany’s involvement in the war in Ukraine. Until recently, the conflict was mainly supported by the United States, which is blamed for its supposed involvement in blowing up Nord Stream 2, the critical pipeline that delivered Russian gas to Germany through the Baltic Sea. The populist Sahra Wagenknecht Alliance (BSW) has made the loss of cheap Russian gas absolutely central to its economic narrative. The party’s overall framing has been that the Zeitenwende (the pivot away from Russia) was an economic debacle driven by ideological alignment with Washington that ran contrary to German national interests.

By contrast, the position of Die Linke has evolved since Wagenknecht split from the left-wing party in 2023. Led by former editor of the German-language Jacobin Ines Schwerdtner, the party has come to frame the energy cost problem as one of corporate power and inadequate social protection rather than as a consequence of breaking with Russia. The leading trade unions and works councils, too, have rhetorically focused mainly on energy prices, but without turning away from a “just energy transition.” Recently, however, breaks in this consensus have appeared. Some trade unions, such as the IG-BCE (covering the mining, chemistry, and energy sectors), seem to be adopting a more critical frame: “We’re supposed to make companies green. We can’t do that when they’re dead,” the IG-BCE head said in 2023.

This emphasis on energy prices is largely unfounded. First of all, a return to pipeline gas from Russia would be by far the most expensive option. The need to repair the pipeline infrastructure, renegotiate contracts under completely different economic conditions, and absorb the sunk costs for the liquefied natural gas (LNG) import infrastructure would render Russian gas far more costly than LNG from Qatar or even the United States. And it is moot: Russian pipeline gas is illegal under new EU laws and a similar ban for Russian LNG is forthcoming.

Moreover, it is not clear that electricity prices explain much the drastic worsening of industrial output and employment in Germany since 2023. An analysis by the German Association of Energy and Water Industries (BDEW) in January showed that the average electricity price for new contracts for small and medium-sized companies between 2023 and 2025 was as low as it was in 2016. This is mainly due to targeted subsidies through reduced electricity taxes and levies, but it indicates that the collapse during this period cannot be attributed to energy costs.

To the extent that higher energy prices did hurt industrial production in previous years — the energy costs of competing industrial firms abroad have fallen in recent years — was largely due to the broader shocks in gas and oil during the pandemic and war. However, the decisive factor in this context was not renewable energies but the blatant German and European general dependence on imports of fossil fuels. The implication is that renewable energy capacity has not been expanded enough.

The argument that the energy transition is to blame is also self-serving. It shields Germany’s political and economic elite from accountability for deliberately damaging the country’s economic prospects. The political class bears collective responsibility for the enormous investment backlog that accumulated during the fiscal consolidation of the 2010s, when they pursued debt reduction through budget balancing despite the fact that interest rates on German government borrowing were very low or even negative. Key infrastructure projects are stagnating, as are private capital investment and capacity utilization, which are further depressed by weak domestic demand in the context of ongoing efforts to reduce debt.

The corporate class, meanwhile, rested on their laurels and were so blinded by their exalted positions in global value chains that they failed to adapt to rapidly changing global markets. No sector embodies this arrogance more than the automotive industry with its rigid adherence to the combustion engine. These failures are an important reason for the fact that the industrial sector in Germany has suffered more than in the rest of Europe, as well as for the loss of competitiveness vis-à-vis their highly innovative and productive Chinese counterparts.

Competition With China

What has been relatively absent from the deindustrialization narrative has been the competition with China, arguably the main cause of industrial employment decline over the last few years. China’s trade surplus (exports minus imports) has grown to over $1 trillion as of 2025, driven both by a growth of exports and a decline in imports, reflecting domestic slowdown and renewed industrial policy efforts in response. Its growth correlates with the decline in German industrial production.

Beyond the large headline trade surplus, the explosive import growth of Chinese motor vehicles to Europe has attracted most of the attention, but this trend is continuing in the other key industries. China’s industrial goods can compete with German products in terms of quality, frequently surpassing them, but are significantly cheaper. The recent drastic shift in competitiveness is not so much due to wage differentials and the highly efficient production lines, but is rather due to the extensive and intensifying network of industrial policy subsidies in China and the currently extremely undervalued currency, the appreciation of which China has been resisting. Both contribute significantly to the fact that Chinese exports are unsurpassably competitive in terms of costs.

It is important to note that China’s enormous trade imbalance does not reflect geopolitical calculus or malicious intent; rather, it shows a growing dependence on net export growth (which is expected to have accounted for over 50 percent of headline GDP growth in 2025) and difficulties in transforming a domestic economy that is currently deflationary and characterized by high youth unemployment into one driven by household demand growth. Overcoming the obstacles to this transformation is the hard political economy problem that China faces.

As far as the energy-transition doomers are concerned, China is the counterargument par excellence. It is the prime example of an industrial miracle that has gone hand in hand with an enormous expansion of solar and wind energy. As it perfected the export-oriented neo-mercantilist model, it also took Germany’s once-vaunted green energy industries to scale. China has gained over 70 percent of market share in the global manufacturing capacity of every major green tech segment, from solar panels to electric vehicles. It annually installs solar energy to the tune of the total capacity of entire economies — and has been doing so consistently for a decade.

If anything, China’s experience shows that there is no connection between the expansion of renewable energy capacity and the decline of heavy industry or complex industrial production. Yet in Germany, much of the party-political spectrum is using the specter of industrial decline as a pretext to mobilize against green energy policies. As for the incumbent: while Merz is aware of the role of trade competition, he apparently still construes it as a regulatory problem and sees an opportunity to implement his unreconstructed neoliberalism: longer working hours, cuts to social benefits, and cuts in income tax.

From the point of view of industrial exports, he is thus pursuing a ruinous race to the bottom, which, against China, cannot be won. Whatever the outcome of his trip to Beijing, it is clear that preventing further decline requires taking a leaf out of China’s book: going all in on renewables and pursuing urgently needed investment-based supply-side and industrial policies.

Wither Atlanticism and Free Trade

Of course, domestic politics will not suffice. A foreign policy realignment, both vis-à-vis China and the United States, is urgently needed. But the “reset in trade relations” that Merz proposed to Xi Jinping requires a clear break with Atlanticism. The relationship with the United States has bound Europe, and thus Germany, to the US policy of escalation toward China. If the renewed momentum, prompted by Donald Trump’s recent threats to annex Greenland, behind pursuing Europe’s “strategic autonomy” from the United States is real, then it should not be squandered.

In addition, the change requires a break with the EU’s neoliberal free-trade ideology: persistent large trade imbalances have consequences and they do not eliminate themselves. In the case of Germany, trade protection measures, such as subsidies and nontariff barriers (for example, regulations that tie Made in EU component shares to state aid), are overdue and they need to be implemented at the level of the European single market. And whatever the trade “reset” with China entails, it must include a new exchange rate policy, one that provides for the steady appreciation of the yuan. China’s blatant dependence on exports means that Europe could use its status as the only large and still open trading bloc as political leverage.

The reshaping of Sino-European relations is the cornerstone of the formulation of what the German physicist and philosopher Carl Friedrich von Weizsäcker referred to as Weltinnenpolitik, or world domestic policy, which internalizes the need to address global problems with the coordination typically associated with domestic politics, rather than through traditional foreign policy or interstate diplomacy. This is the sufficient condition for avoiding a disorderly deindustrialization and long-term transformation of Germany into a service society characterized by the extreme inequalities and social deprivation associated with the Anglo-American model.