“Raising the Retirement Age” for Social Security Just Means Cutting Benefits

GOP leaders say they want to raise the Social Security retirement age. That’s just a deceptive way of saying they want to cut benefits — punishing nonwealthy Americans while leaving untouched the massive government spending on tax shelters for the rich.

Republican House minority leader Kevin McCarthy and Senate minority leader Mitch McConnell. (Nicholas Kamm / AFP via Getty Images)

Republican leaders have recently suggested that they would use a debt ceiling showdown to force cuts to the Social Security program. Democrats should get ahead of this by eliminating the debt ceiling right now. If Democrats don’t do that, then President Joe Biden should simply ignore the debt ceiling when the time comes. Neither counteraction seems likely to happen, so a debt ceiling showdown involving Social Security negotiations is quite likely to happen if the Democrats lose control of the House or Senate in the midterm elections.

The Social Security reform discourse frequently revolves around the idea of increasing the Social Security retirement age. But this discourse is a bit misleading in ways that tend to to obfuscate what proponents of that idea are actually proposing.

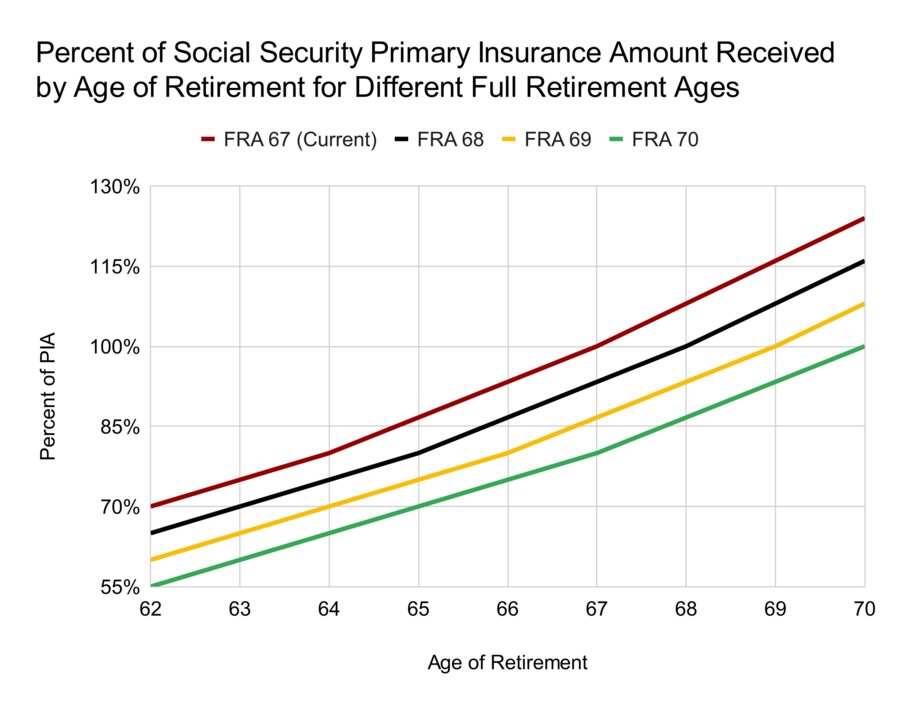

Social Security does not have one retirement age. It has ninety-six retirement ages, one for each month between age sixty-two and seventy. What people call the “full retirement age” (FRA) is just a placeholder in a formula that determines the benefit level at all ninety-six retirement ages.

People who retire at the FRA receive 100 percent of the “primary insurance amount” (PIA), which is a dollar figure derived from a formula applied to each individual’s earnings record. People who retire before or after the FRA receive less or more than 100 percent of the PIA based on how far away from the FRA they are when they retire.

In the below graph, we can see what these percentages are at all ninety-six retirement ages when the FRA is set at age sixty-seven (the current FRA), age sixty-eight, age sixty-nine, and age seventy.

When someone proposes increasing the retirement age to sixty-eight, all they are really proposing is to cut monthly Social Security benefits by around 7 percent at all ninety-six retirement ages. A proposal to raise the retirement age to seventy is just a proposal to cut monthly benefits by around 23 percent at all ninety-six retirement ages. None of this is about when you retire. It’s just a straightforward benefit reduction being expressed in an opaque way.

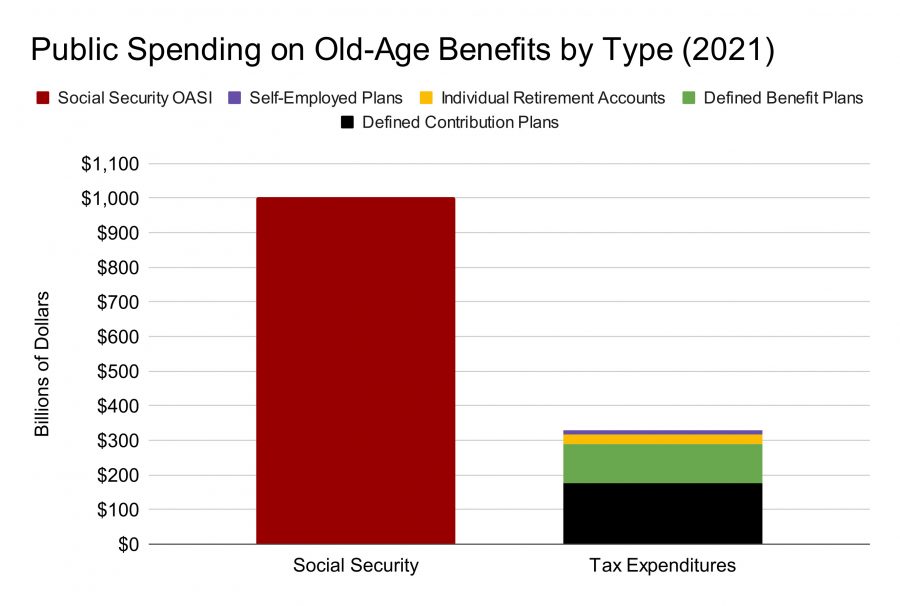

Another remarkable thing about the Social Security discourse is that it proceeds as if Social Security is the only way that the federal government provides old-age income support. But this is not the case. In 2021, the federal government spent a little over $1 trillion on old-age and survivors insurance (OASI). In the same year, it spent $329 billion on tax expenditures for private retirement accounts and pensions.

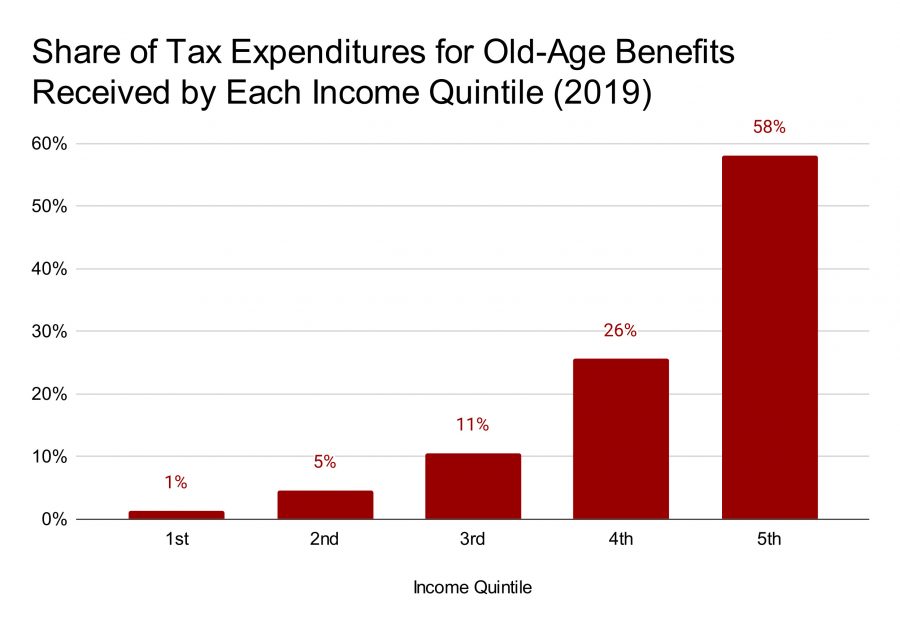

These tax expenditures benefit affluent Americans far more than nonaffluent Americans. In 2019, the Congressional Budget Office (CBO) estimated that the richest 20 percent of Americans received 58 percent of these old-age tax expenditure benefits while the poorest 20 percent of Americans received 1 percent of them.

This distributive skew is built in to the way that these tax expenditures work. As the CBO explains:

Higher-income taxpayers tend to benefit more from the exclusion for pensions and retirement savings accounts for three main reasons. First, such taxpayers are more likely to have employers who offer pension plans and who are also more likely to contribute to retirement savings accounts. Second, the generosity of such plans and contributions increases with income, although that effect is limited by caps on contributions and antidiscrimination rules that prevent employers from making retirement plans significantly more valuable for highly compensated employees than for other employees. Finally, higher-income taxpayers face higher marginal tax rates — that is, the tax rate that would apply to an additional dollar of income — which increases the value of the tax expenditure for each additional dollar of their retirement savings.

If one really believed that federal spending on old-age benefits was out of control, clearly the first place to cut would be from the $329 billion spent on these tax expenditure programs that primarily operate as a tax shelter for the capital income of the rich. This could be accomplished by lowering contribution caps, lowering what percent of each contribution can be used toward tax deductions, or, better yet, scrapping the IRA/401k system as a whole.

Despite the fact that this private side of our retirement system is vastly worse than the Social Security program, high-level policy fights about aging and retirement proceed as if it doesn’t exist or is untouchable. This is because the fights are not really about retirement security but are instead about using the retirement security system to grind ideological axes about the welfare state and capital taxation.