Calm Down, Mass Inflation Is Not Around the Corner

The frenzied warnings of impending mass inflation are completely overblown. The inflation we've seen has been limited to a few specific items — and putting the brakes on the economy now would hammer the working class.

Sen. Roger Marshall (R-KS) holds up a hundred-dollar bill during a press conference on inflation held by Republican senators on Capitol Hill on May 26, 2021. (Drew Angerer / Getty Images)

The Bureau of Labor Statistics released its monthly inflation report a couple of weeks ago. The headline statistic is that prices increased by 4.2 percent from April of last year and 0.8 percent from the prior month. Taken alone, these headline numbers might cause alarm for some, but once you dig into the report, you find that these increases are not primarily driven by general price rises across the economy but instead by price rises for three specific items: hotels, airline fares, and used cars.

When analyzing inflation trends, it’s common to start by focusing down on core inflation, which refers to all of the items in the Consumer Price Index (CPI) except for energy and food. The items in the core inflation basket make up 79 percent of the entire inflation basket and the core inflation rate rose by the same amount as the overall inflation rate: 0.8 percent between March and April.

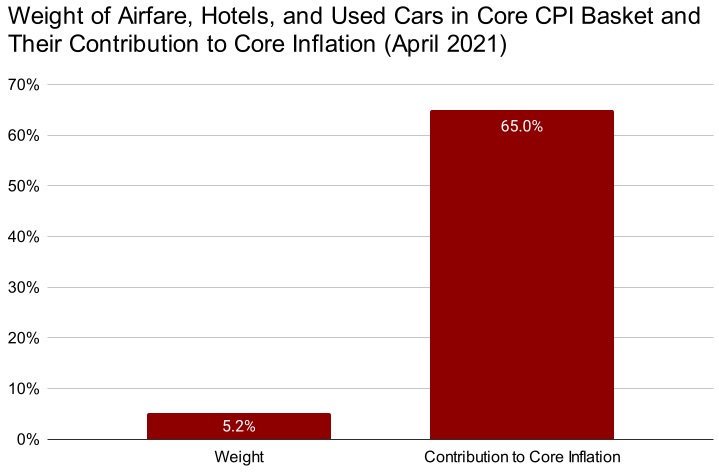

A glance at the detailed expenditure categories included in the core inflation basket reveals that hotels, airfares, and used cars drove the supermajority of inflation over the last month. These items make up just 5.2 percent of the core inflation basket but accounted for 65 percent of core inflation.

The fact that airfare and hotel prices rose a lot last month likely indicates a big spike in travel driven by spring break and coronavirus vaccination. These two industries are also much more reliant on dynamic pricing (aka surge pricing), meaning that demand surges in those sectors are going to be more readily reflected in prices.

The main explanation people have given for the used car spike is that new car production has declined, and the reason new car production has declined is that there is a shortage of the semiconductor chips that are used to power the electronics of new cars. With fewer new cars in the pipeline, car buyers are turning to the used car market, pushing up prices.

Another reason given for the new car shortage is that carmakers spun down production during the recession, with some even repurposing plants to make coronavirus-related medical devices, and they have not been able to quickly retool their plants to meet the demand spike for cars. Indeed, this is also sometimes given as the reason for the shortage in semiconductor chip production: when car makers spun down production during the recession, they stopped ordering semiconductor chips, and when they did that, semiconductor makers spun down their production and have been slow to get that production back up.

In any event, it’s not the case that used car prices are increasing due to an escalation of wages or other producer prices in the used car sector: used cars have already been produced.

Nothing about this picture suggests that spending and inflation are out of control in a general sense. And it would be obviously ridiculous to throttle the macroeconomy in order to bring down prices on these three items.

Airlines and hotels can respond to demand surges by running more flights and opening more rooms. Or, if they can’t, then it’s perfectly fine for them to increase the price level of the scarce flights and rooms they have in order to clear the market. Such price hikes are one-off measures, not accelerating inflation.

The used car problem, which is really a new car problem, which is really a semiconductor problem, needs to be addressed by bringing the semiconductor capacity back online, if you believe the industry reporting on the matter. And higher prices provide precisely the kind of signal and incentive that investors and firm managers are supposed to respond to.

It is certainly possible that inflation will kick up problematically at some point in the near future, but it is wrong to suggest that it has already, and it would be especially wrong to push down demand in order to try to tackle inflation at this moment.