In 2021, Larry Summers Won the Inflation Debate. But His Victory Was Transitory.

With price growth trending down over the past year despite a strong labor market, it’s looking more and more like Larry Summers was wrong about inflation after all. It’s time to revisit the great inflation debate of 2021–2022.

Former treasury secretary Larry Summers attends the official White House portrait unveiling ceremony for President Barack Obama and former first lady Michelle Obama in the East Room of the White House on September 7, 2022. (Tom Williams / CQ-Roll Call, Inc via Getty Images)

Larry Summers’s “victory” in the Great COVID Inflation Debate can be dated quite precisely: it came on November 22, 2021. That’s when Jerome Powell announced that the Federal Reserve would stop characterizing high post-COVID inflation rates as “transitory.” The announcement was largely symbolic, of course. But it was part of a broader Fed policy U-turn that followed months of accelerating price rises and mounting criticism from the likes of Summers, who had been flagellating the Fed for its alleged nonchalance on inflation.

Since that date, the media have treated the former treasury secretary as an oracle: the man who saw it all coming. Just a week before Powell’s announcement, Summers’s column in the Washington Post had borne the snarling, alpha-male headline: “On inflation, it’s past time for team ‘transitory’ to stand down.” And lo, “team transitory” — meaning those at the Federal Reserve and elsewhere who had been predicting that high post-COVID inflation rates would go away on their own without the need for a recession — by and large stood down.

Since he first started sounding the inflation alarm in early 2021, the core of Summers’s argument has been that Biden’s stimulus, combined with the Federal Reserve’s failure to promptly counteract its effects with monetary tightening, had overheated the economy, and that unless the Fed engineered a sharp rise in unemployment (and most likely a recession) to quash the resulting inflationary dynamic, high inflation would become entrenched, eventually forcing the Fed to take even harsher action down the road.

But then a funny thing happened. Inflation peaked in early 2022, and over the course of the year it followed a steady and broad-based downward trend. The inflation rate as measured by the Consumer Price Index (CPI) was 9.7 percent annualized in the second quarter, 5.5 percent in the third quarter, and 4.2 percent in the fourth quarter. In the last two months for which we have data (November and December 2022) the rate averaged 2 percent. Most importantly — and in stark contrast to Summers’s prognostications — this happened in the absence of any spike in unemployment. In fact, the labor market has continued to surprise analysts with its strength.

Reacting to a series of favorable data releases earlier this month, Summers, who spent 2021 denouncing Biden’s stimulus policies in the most splenetic terms — “the least responsible fiscal, macroeconomic policy we’ve have had for the last forty years” — had to lamely acknowledge that those policies “will look much better than I thought six months ago” if the current trend of falling inflation without rising unemployment continues.

While there isn’t yet anything like a consensus, it seems increasingly likely (to me, at least) that posterity will judge Summers to have been wrong and his bête noire, “Team Transitory,” right about inflation after all. A recession might still come, thanks to the Fed’s aggressive monetary tightening. And there will undoubtedly be bumps on the road of disinflation. But there has been no meaningful softening in the labor market thus far, and yet inflation pressures have been rapidly easing anyway. That’s exactly what it means for inflation to be “transitory,” in the specific sense in which that word is used in policy debates. So I vote for taking Summers’s trophy back.

But if Summers and his fellow hawks were wrong, why were they wrong?

In March 2021, Summers offered a glimpse of how he thought about the current inflation problem. In an appearance on Bloomberg TV, he said:

I’m concerned that we’re having a dynamic that is in many ways reminiscent of the 1960s, when conflicting demands, great social concern, led well-intentioned officials — terribly dedicated, serious, and thoughtful officials — to be too optimistic about what the economy could handle, and let things get away from them. And inflation went from 2 percent in 1966 to 6 percent in 1969, before there were any supply shocks. It seems to me that we’re at risk of making that kind of mistake.

At the time, I thought this sort of thinking was anachronistic. In an article that October, I argued that the kind of inflation the capitalist world experienced in the 1960s and 1970s — in fact, throughout the whole “short twentieth century” that was bookended by World War I on one side and the collapse of the Soviet Union on the other — was “a historical phenomenon from an earlier phase of capitalism. It emerged in the interwar period. Its existence was discovered by the public and the economics profession quite suddenly in the late 1950s. And then, sometime between 1985 and 1995, it ended.”

Now seems like a good time to flesh out that argument, which is what I’ll do below and in a few follow-up articles. Readers will probably notice that the view of inflation presented below seems — at least on the surface — to be in dissonance with those of many economists on the Left who’ve been writing about inflation over the past two years. Whether that clash is just cosmetic or represents a deep difference of analysis is an open question — and possibly a topic for another article.

Demand, Wages, and Inflation

Inflation is a complicated subject, but there’s one theory of prices everybody knows, even if they know nothing about economics: holding all else equal, when the price of something goes up, less of it is bought. This simple idea goes by a pretentious name: the Law of Demand.

The Law of Demand is an equilibrating tendency. Just as a thermostat equilibrates the temperature of a room, so that anything that heats or cools the room (say, sunlight pouring in through a window) triggers a countervailing response from the thermostat, anything that puts upward pressure on the price of a product — say, an accident that disables an oil refinery, pushing up the cost of airline flights and road trips via higher fuel prices — triggers a countervailing response from the public: fewer airline tickets are purchased, fewer road trips are taken, and production demands on the remaining oil refineries are correspondingly eased. Soon enough this puts an end to the upward movement of fuel prices.

In COVID-era discussions of inflation, somehow this most elementary fact about the price mechanism always seemed to get lost. But it’s actually crucial: whenever there’s concern about rising prices, a good first question to ask is why the problem shouldn’t be left to resolve itself on its own through the self-regulating mechanics of supply and demand. If the prices of products are accelerating, won’t people respond by buying fewer products? And won’t this put an end to the inflation?

The answer to both of these questions is yes — unless incomes are accelerating, too. If prices go up but incomes don’t, the volume of goods people can buy with their incomes falls; if the volume of buying declines, inflation tends to subside. No advanced economics training is needed to grasp these points. Simply put, you can’t have continually rising prices unless people are able to pay them.

This is what makes the wage — or rather the rate of wage growth — so central to the determination of the price level. Wages possess the unique property of being simultaneously the main source of production costs for firms (supply) and also the main source of purchasing power for the customers of those firms (demand).

It’s this symmetry that enables the wage to, in a manner of speaking, sidestep the equilibrating force of the Law of Demand: by increasing production costs, a higher wage level induces firms to raise their prices; and by increasing the level of incomes, it makes it possible for those higher prices to be sustained without triggering an equilibrating countermovement.

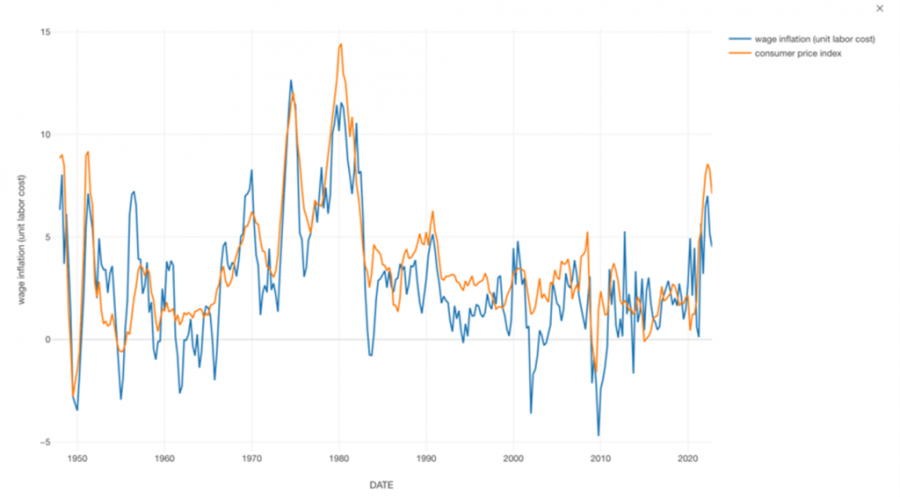

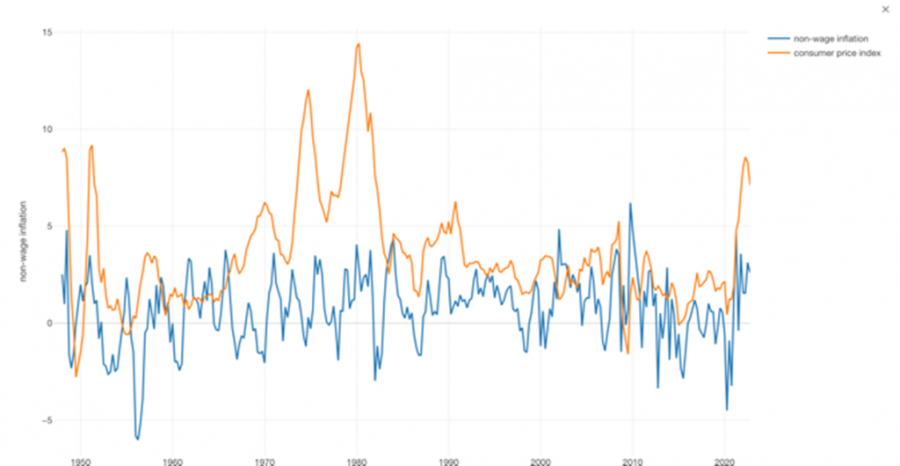

The close connection between inflation and wage rates — or, more precisely, between inflation and unit labor cost (ULC), which is wage growth relative to labor productivity — is blatant in the data. In the two following charts, the link is illustrated with a very simple accounting exercise. The inflation rate, as measured by the CPI, is separated into two components: the part accounted for by the growth of ULC, which I’ve labeled “wage inflation,” and the residual left over after subtracting the rate of ULC growth from the inflation rate, which I’ve label “non-wage inflation.”

In the first chart, the total CPI inflation rate is plotted against its wage-inflation component (i.e., ULC growth); in the second chart it is plotted against the non-wage inflation component (the residual).

What these charts show is that while wage and price inflation rise and fall quite closely in step with each other — with wage inflation high during periods of high inflation and low in times of low inflation — non-wage inflation just fluctuates directionlessly, around a long-run average close to zero (in this example, about 0.7 percent).

In other words, high wage inflation is a reliable predictor of high price inflation, but the same doesn’t hold for non-wage inflation: when non-wage inflation is unusually high, that mainly just signals that it’s due for a mean-reverting decline.

I’m not claiming it’s some kind of secret that wages are an important factor in inflation. You just have to read the news, which, as I write, is full of talk about Jerome Powell’s latest musing on the wages-inflation link.

But from early on in the COVID-era inflation resurgence, a grossly misleading picture of the problem was conveyed in reporting and commentary because of a failure to give due attention to the obverse side of this point: that in the absence of inflationary wage growth, price inflation is inherently self-limiting. In other words, transitory.

Keynes and the Quantity Theory of Money

The view of inflation stated above, with its stress on the role of wage growth, might not meet with universal approval, but one thing, at least, can be said for it: it was the view of John Maynard Keynes and his closest collaborators. And the fact that it was their view is another point that has gotten lost in recent discussions of inflation.

“The essence of inflation is a rapid and continuous rise of money wages. Without rising money wages, inflation cannot occur, and whatever starts a violent rise in money wages starts inflation.”

Those lines were written in 1938 by Joan Robinson, the original “left-wing Keynesian” (her term), and by all accounts one of the twentieth century’s greatest economists, in a review of a book on Germany’s post–World War I hyperinflation.

Robinson and the other apostles of Keynes never ceased to insist on this analysis of inflation. It was a theoretical cornerstone of the new economics they were pioneering at the University of Cambridge at the moment she wrote those lines. The idea was summarized by Keynes’s former student Richard Kahn, who, along with Robinson, formed the innermost ring of Keynes’s Cambridge “circus”:

The money wage is the fulcrum on which rests the whole structure of everything expressed in terms of money — all prices, incomes of every kind, and all money values. A higher level of money wages means that everything expressed in terms of money is higher in the same proportion.

Until that point, all the reigning theories of inflation had been based on that ancient totem of orthodoxy, the Quantity Theory of Money, the longest-extant theory in economics. The quantity theory had undergone endless metamorphoses and revisions over the centuries (its earliest formulations date as far back as the sixteenth century, when torrents of Spanish New World silver were driving up European prices), but in all of its versions it always posited a close, causal relationship between the quantity of money in circulation and the overall price level — with causation running strictly from the former to the latter.

During its nineteenth-century career as an intellectual buttress to Victorian laissez-faire, the quantity theory functioned in tandem with Say’s Law, the proposition that free markets automatically tend toward full employment so long as prices and wages are left free to adjust to one another. When combined, the two notions yield the so-called classical dichotomy — the view that money is one thing and production another thing, and that neither has any long-run effect on the other.

The quantity theory was thus bound up with a pervasive nineteenth-century worldview that regarded outcomes in the “real economy” — the level of employment, the allocation of productive capital, and so on — as reflecting the beneficent efficiency of supply and demand, flowing from acts of individual choice and private competition and directed by movements in relative prices. This worldview regarded money with suspicion, as an inevitably collective institution that, at best, could neutrally facilitate exchange, but at worst stood always ready to disrupt and disorganize economic life through mismanagement of the printing press (or the banking system) — a malady that manifested itself via swings in the absolute price level.

In its most sophisticated versions, the quantity theory rested on the assumption that, since money has no intrinsic value and pays no interest, the only reason anyone would willingly hold part of their wealth in the form of money (as opposed to more remunerative forms, like bonds or real estate or automobiles) is to facilitate ordinary purchases of goods and services. The idea seems straightforward: keeping some amount of cash always on hand obviates the need to, say, sell a bond from your portfolio every time you go to supermarket.

If that were, in fact, the only reason to hold money, the “demand for money” would be a highly stable and predictable variable, moving closely in step with the volume of aggregate spending (i.e., GDP). And if the demand for money is stable and predictable, any large or sudden changes in the value of money — inflation or deflation — would have to be chalked up to changes on the supply side, i.e. the quantity of money. That was the logic of the quantity theory.

Keynes was practically born into the intellectual tradition of the quantity theory; he imbibed it as mother’s milk from Alfred Marshall, his scholarly master at Cambridge (and a close family friend) who had played a central role in formulating the theory’s modern neoclassical version. As late as 1930 Keynes still clung to his identity as a quantity theorist in some loose sense.

But in the early 1930s, strongly influenced by discussions with Kahn, who harbored an almost lifelong distaste for the quantity theory, Keynes concluded that its core assumption of stable money demand was irreparably flawed.

Once it’s understood that money is held not just to facilitate a more or less predictable flow of spending, but also as a hedge against a fundamentally unknowable future — a point to which Keynes attached great significance — the money-demand variable loses its predictability and stability and it can no longer be assumed that swings in the value of money are caused solely by changes in its supply, or that changes in the supply of money will necessarily alter its value in any predictable way.

Hence Keynes, in his preface to the French edition of his General Theory of Employment, Interest and Money, called the book “my final escape from the confusions of the Quantity Theory, which once entangled me.” Rather than look to the dynamics of money, he would now regard the price level “as being determined in precisely the same way as individual prices; that is to say, under the influence of supply and demand” (for goods and services).

That’s why Keynes laid such stress on the inflation-determining role of the wage rate, with its preponderant influence on both supply and demand. Of course, this wage-inflation link was freighted with heavy social and ideological implications. I’ll be getting into that in my next piece.