The US Tax Code Should Not Allow Billionaires to Exist

The recent ProPublica exposé about billionaires’ almost-nonexistent tax bill was just the latest to reveal how little the ultrarich pay in taxes. We need to attack the wealth and power of the rich — and that means massively increasing taxes on them.

Amazon CEO Jeff Bezos is the richest man in the world. (Elif Ozturk / Anadolu Agency via Getty Images)

Last month, ProPublica highlighted the gross inequities of the US tax system with an exposé that drew on the leaked tax returns of the country’s billionaires. It showed that the wealth of the twenty-five richest Americans grew by a combined $401 billion from 2014 to 2018, but that they paid only 3.4 percent of that sum in federal income taxes. Over the same period, the average American paid more in federal taxes than they gained in wealth.

ProPublica’s president called the tax investigation the “most important story” in the outlet’s history. The report went viral on social media and received coverage in virtually every major news outlet. Many observers predicted the story would spur legislation. As the Center for Budget and Policy Priorities’ Chuck Marr tweeted, “There should and will be strong pressure on policymakers to act to respond to what the public will correctly perceive as a gross unfairness.”

ProPublica’s piece — which actually understated the regressivity of the US tax code — should be a political gift to Democrats that spurs meaningful policy change. But the past century has seen similar exposés every decade or so, and they’ve rarely produced a substantial legislative response. Time and again, the ultrarich’s well-funded army of sycophants and bipartisan gallery of politicians have come to the rescue to ensure America’s plutocrats continue to escape taxation.

Will this time will be different?

The Pecora Hearings

Perhaps the earliest precursor to ProPublica’s article — and the only instance of tax revelations triggering meaningful legislation — came in the early years of the Great Depression. In the course of investigating Wall Street’s role in the stock market crash of 1929, the Senate Committee on Banking’s chief counsel, Ferdinand Pecora, discovered that J. P. Morgan Jr — one of the richest men in the country and a poster boy for unearned, dynastic wealth — paid no federal income taxes in 1931 and 1932.

The revelations made front-page news in the New York Times and across the country. The New Republic summarized the reaction: “What has rankled most in the hearts of the vocal public is that when millions of persons with small incomes were straining every nerve to meet their income taxes, these princes of wealth, who personally enjoyed luxuries denied to almost everyone else, did not pay any income tax at all.”

Among those cheering on Pecora’s vivisection of Morgan and the tax laws that enabled his profligacy was President Franklin Roosevelt. In response to the Pecora hearings (and the political challenge represented by Huey Long’s “Share Our Wealth” program), Roosevelt proposed what became the Revenue Act of 1935. In announcing his proposals, FDR cast the legislation in populist terms:

Our revenue laws have operated in many ways to the unfair advantage of the few, and they have done little to prevent an unjust concentration of wealth and economic power. . . . Wealth in the modern world does not come merely from individual effort; it results from a combination of individual effort and of the manifold uses to which the community puts that effort. . . . A tax upon inherited economic power is a tax upon static wealth, not upon that dynamic wealth which makes for the healthy diffusion of economic good. . . . Therefore, the duty rests upon the government to restrict such incomes by very high taxes.

Opponents decried FDR’s proposals as “soak-the-rich,” but the criticism only underscored their populist appeal. Ultimately, the Revenue Act of 1935 increased the top federal income rate on incomes over $1 million from 59 percent to 75 percent, created a graduated corporate income tax, and raised estate taxes.

While modern critics of FDR’s policies argue that these measures were largely symbolic, they did meaningfully boost effective rates on the ultrarich and initiated the cascade of progressive taxation that reigned through the 1950s — curbing the political and economic power of the rich and raising the incomes of the working- and middle-classes more than those of the affluent.

Exposes and Inaction

In December 1962, in a speech before the Economic Club of New York, President John F. Kennedy signaled the beginning of the end of New Deal–style taxation. Kennedy argued that the progressive tax system created by FDR and his allies “reduce[d] the financial incentives for personal effort, investment, and risk-taking” and “deterre[d] . . . private initiative,” which he promised to fix with “an across-the-board, top-to-bottom cut in personal and corporate income taxes.” Kennedy also predicted that slashing taxes would actually increase revenue, a claim later adopted by Republicans.

In 1981, Ronald Reagan invoked the Kennedy-Johnson legislation when pushing his own top-heavy tax cuts, and Republicans continually named JFK as the original supply-sider in the decades that followed. While liberals have bristled at these comparisons, it’s the rare case where conservatives’ interpretation of history comes closer to the truth.

The Department of Commerce’s analysis showed that the rich benefited the most from the Kennedy-Johnson tax changes. The combination of these federal cuts with increases in regressive state and local taxes meant that taxes on the rich fell while taxes on the poor rose during the Democratic trifecta of the early ’60s. The Kennedy-Johnson law, in short, created the basic distributional pattern that Republicans would emulate (and exacerbate) in the decades between Kennedy and Trump.

Those decades witnessed a deluge of exposés illustrating the unfairness of the tax code. The early-to-mid ’60s alone saw popular books from law professor Jerome Hellerstein (Taxes, Loopholes, and Morals) and former Democratic congressional staffer Philip Stern (The Great Treasury Raid), along with articles from the likes of Senator Albert Gore, Sr and muckraking journalist Jack Anderson, among others.

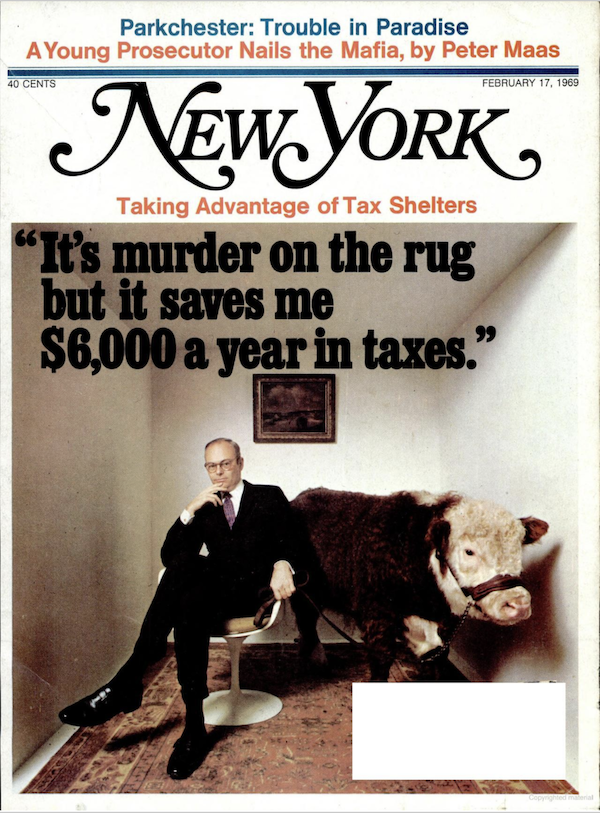

By the end of the decade, reports on loopholes benefitting the rich were commonplace in newspapers and magazines, a trend exemplified by a provocative February 1969 New York magazine cover story on the use of tax loss farming schemes by everyone from celebrities to Wall Street execs.

Ultimately, the country’s closest brush with meaningful tax reform came not as the result of journalistic investigations, but from revelations made by Johnson’s outgoing treasury secretary, Joseph Barr. Just weeks before the New York magazine article, Barr announced that “in the year 1967, there were 155 tax returns in this country with incomes over $200,000 a year and 21 returns with incomes over a million dollars a year on which the ‘taxpayers’ paid the U.S. government not one cent of income taxes.”

Barr’s testimony made headlines and prompted what columnists Rowland Evans and Robert Novak called “torrents of spontaneous mail demanding tax reform.” However, the resulting Tax Reform Act of 1969 did little to close the loopholes that allowed the rich to escape taxation, causing the New York Times to dub it “a mouse of a reform bill.”

Attention to tax loopholes only increased in the 1970s. Both consumer crusader Ralph Nader and National Welfare Rights Organization founder George Wiley formed their own tax groups. Nader’s Tax Reform Research Group published a monthly muckraking newsletter, “People & Taxes,” while also churning out report after report outlining tax provisions that benefitted the rich at every level of government. In 1973, Philip Stern scored another bestseller with his unfortunately titled Rape of the Taxpayer: Why You Pay More and the Rich Pay Less.

“The Tax Laws Are Written to Help the Rich”

Meanwhile, Republicans inadvertently fanned the flames of tax resentment with their personal scandals. In May 1971, Rosemarie King, a student journalist at Sacramento State, reported that California’s then-governor, Ronald Reagan, had paid no state income taxes in 1970. The report set off a string of revelations showing that Reagan — who famously quipped “taxes should hurt” when opposing state income tax withholding — paid neither state nor federal income taxes, despite a gubernatorial salary that alone placed him in the top 1 percent nationally.

Two years later, President Richard Nixon became embroiled in a tax scandal of his own when an unnamed IRS employee leaked Nixon’s tax returns to the Providence Journal’s Jack White, who won a Pulitzer Prize for the story. The returns showed that Nixon paid under $800 in federal income taxes in 1970 and less than $900 in 1971, despite more than $250,000 in income.

In the wake of these revelations, three-quarters of Americans told a congressional survey that they believed “the tax laws are written to help the rich, not the average man.”

But rather than spurring an FDR-esque round of progressive reform, the revelations and public outrage bore no meaningful legislative fruit. Instead, President Jimmy Carter — who ran in 1976 on a platform of progressive, loophole-closing tax reform — signed the Revenue Act of 1978, which shrunk the effective top rate on capital gains to a paltry 28 percent and handed 90 percent of its benefits to the top 10 percent of taxpayers. Reagan’s famed 1981 cuts simply finished the funneling of money to the rich that Carter began three years earlier.

When DC finally got around to tax reform in 1986, lawmakers sought to “broaden the base and lower the rates,” a philosophy that amounted to compensating the rich for closed loopholes by lowering the statutory rates on high incomes. Thus, the top income tax rate of 50 percent was brought down to the 28 percent rate that applied to capital gains following Carter’s cut, rather than the other way around.

In the end, the Tax Reform Act of 1986 did little to alter the distribution of taxation in the United States. It signaled, as scholar Michael Graetz put it, “the demise of progressivity as the guiding principle for fairness in the distribution of tax burdens in the federal tax system.” Precisely because the Tax Reform Act of 1986 failed to make the rich pay their fair share, it’s become the platonic ideal of tax reform in the minds of conservatives and centrist Democrats alike.

As tax rates dropped, muckraking tax reporting continued unabated. Reporter David Cay Johnston garnered a Pulitzer Prize for a series of articles in the 1990s and 2000s on regressive tax loopholes, then published the bestselling Perfectly Legal: The Covert Campaign to Rig Our Tax System to Benefit the Super Rich — and Cheat Everybody Else in 2003. (In 2017, Johnston made headlines again by providing the public with its first peak at President Trump’s tax-avoiding returns.)

All the while, taxes on the very rich continued to go down — a long-term trend only interrupted by Democratic presidents’ occasional partial repeals of Republican tax cuts (which were then undone, and then some, by the next Republican in the White House).

Today — as both ProPublica’s report and IRS data compiled by economists Thomas Piketty, Emmanuel Saez, and Gabriel Zucman demonstrate — taxes on the ultrarich are as low as they’ve ever been.

If Biden truly wants an “FDR-sized” presidency, he’ll have to follow FDR’s lead in pressing his corporate-friendly colleagues to pass progressive tax reform.

Wealth for Whom?

While hiking taxes on the rich is overwhelmingly popular, and the GOP’s regressive tax cut agenda holds little public appeal, many Democrats still haven’t grasped that they should be forcing Republicans to spend the next year and a half before the midterms explaining why they think Jeff Bezos should pay a lower tax rate than an Amazon warehouse worker.

Before ProPublica’s piece, some Democrats were even balking at Biden’s modest proposals to hike taxes on corporations and the wealthy, which — while bolder than Obama’s tepid plans — still fall well short of what’s needed to meaningfully curb the economic and political power of the 1 percent.

Thanks to the likes of Virginia’s Mark Warner, New Jersey’s Bob Menendez, and West Virginia’s Joe Manchin, among other right-leaning Democrats, big businesses and wealthy individuals haven’t exactly been concerned that the tax man is coming for them.

As Politico noted in May, “Interviews with over a dozen executives, lobbyists and business group officials turned up a similar theme: While Democrats might be able to push through a slightly higher top corporate rate, when it comes to higher taxes on the rich, on capital gains, on financial transactions or private equity profits, forget it. It’s not happening.”

At least temporarily, the ProPublica report — and subsequent stories by the New York Times and Mother Jones on tax avoidance by private equity firms and wealthy individual’s estates — placed Republicans and conservative Democrats on their back foot. The day ProPublica’s investigation hit the web, the usual defenders of plutocracy sputtered to mount coherent defenses of Bezos and company’s paltry tax payments.

Right-wingers’ first response was to attempt to shift the discussion from the contents of the billionaires’ tax returns to the leak of the information. The archconservative Wall Street Journal editorial board whinged that “the real scandal . . . is that someone leaked confidential IRS information about individuals to serve a political agenda.”

Libertarian economist Tyler Cowen, the head of the Koch-funded Mercatus Center at George Mason University, groused that “ProPublica acted unethically” and wildly speculated that “the Russians” were behind the leak. Major conservative outlets like Fox News echoed this line of attack on the ProPublica piece, and elected Republicans likewise worked to turn the leak itself into the story, with Senate Minority Leader Mitch McConnell declaring “whoever did this ought to be hunted down and thrown into jail.”

Other critics focused on ProPublica’s “true tax rate” concept. In order to capture the fact that a billionaire’s wealth can increase almost exponentially without generating any taxable gains in a given year, ProPublica’s journalists divided the taxes each billionaire paid in a certain year by how much their wealth increased that year. They did the same for average Americans. This isn’t, of course, how US tax law currently defines income. Bloomberg writer Noah Smith quipped on Twitter, “Americans shocked, SHOCKED, to discover that capital gains tax only gets paid when you sell.” However, this response is nothing more than a pseudo-clever gotcha.

ProPublica’s report made clear that it needed to devise a new tax measure because the US tax code currently lets the ultrarich accrue almost unlimited wealth tax-free. Indeed, its report focuses on the “buy, borrow, die” trifecta used by the wealthy, whereby they accrue wealth, fund their lavish lifestyle by borrowing against that wealth tax-free, then pass along the windfall to their heirs using the “stepped up basis” (or “step up in basis”) loophole, which ensures capital gains taxes will touch little of it.

The crux of the issue was made plain by, of all people, Mark Cuban, the billionaire owner of the Dallas Mavericks, who asked, “Do you tax net worth or do you only tax income?” Cuban insisted that its almost un-American to tax wealth as its accrued.

Yet wealth is only out-of-bounds in elite political discussions when it comes to the 1 percent. Working-class and middle-class Americans, on the other hand, are well-acquainted with a yearly tax on their main source of wealth: their home.

According to a comprehensive analysis by economist Edward N. Wolff, a principal residence composes more than 60 percent of the gross assets of the middle 60 percent of households. For the top 1 percent, that share is less than 8 percent. Meanwhile, 80 percent of the wealthiest 1 percent’s assets come from investments and business equity. The same share for the middle 60 percent is less than 15 percent.

Because of the widespread use of the property tax by states and localities, the non-rich pay taxes on their biggest source of wealth every year. The owner of a $217,500 home (the median value nationally) can expect to pay nearly $2,500 on average in property taxes every year. In states like Illinois and New Jersey, the yearly total climbs to nearly $5,000. That means that over the course of a thirty-year mortgage, the average homeowner will shell out nearly one-third of their house’s purchase price in property taxes.

But even that figure undersells the yawning gap between how we tax houses and other forms of wealth. The average homebuyer puts down only around 10 percent of their home’s price, meaning that in most years a homebuyer is paying taxes on the full value of a home, despite equity that amounts to only a tiny fraction of that. As Wolff’s data shows, the top 1 percent’s debt-to-income ratio is 35 percent, while the middle 60 percent’s debt-to-income ratio is a whopping 120 percent — almost three times the ratio necessary for a qualified mortgage.

The Need for a Populist Tax Attack

Progressive tax reformers have proposed taxing the increase in the wealth of the rich each year through “mark-to-market” valuation. Unsurprisingly, conservatives have objected with arguments similar to those they made against ProPublica’s “true tax rate,” namely that valuing assets yearly is unfeasible and unfair to (rich) investors.

Yet this is precisely what we do with homes each year, with the crucial difference that average homeowners are taxed not merely on the gain in value of the fraction of the home they own, but on the full value of the home, regardless of whether they own it outright or have less than 10 percent equity.

As a result, property taxes are enormously regressive. According to the Institute on Taxation & Economic Policy, the poorest 20 percent of households pay an effective property tax rate of 4.2 percent, while the top 1 percent pay an effective rate of 1.7 percent. This regressivity is exacerbated by an assessment process that’s biased against lower-income homeowners and homeowners of color.

According to a University of Chicago study, “a property valued in the bottom 10% within a particular jurisdiction pays an effective tax rate that is, on average, more than double that paid by a property in the top 10%.” Nor do renters escape the bite of the property tax: landlords pass along their property taxes in the form of higher rents.

Ultimately, both the low taxes on the rich and the feigned helplessness of business-backed lawmakers are just another sign of America’s culture of impunity for elites and discipline for the have-nots — where if you’re the wrong class or color you’re liable to be thrown in jail for unpaid parking tickets, but if you’re a 1 percenter, you can get off scot-free for far more serious crimes. Reinstating the steep progressive taxation of the mid-twentieth century is crucial to reshaping the United States’ deformed economy and political culture.

The ProPublica report has handed Democrats ample ammunition for a populist tax attack that could finally begin to roll back the wealth and power of the rich. The question, as it has been for the past half century, is whether they will use it.